The Economy Macro-Cap : India's BoP outlook improves by Motilal Oswal Financial Services Ltd

* Key Takeaway: The monetary policy announced last Friday (5th June link) marked a significant policy turnaround, given its impact on foreign capital inflows. The RBI announced a series of measures to attract foreign capital inflows, including:

* Absorbing the hedging cost on fresh FCNR (B) deposits. These deposits are mostly exempted from the cash reserve ratio (CRR) and statutory liquidity ratio (SLR) requirements, which is positive for both bank liquidity and credit offtake

* Enabling banks to offer attractive deposit rates to NRIs

* Encouraging PSUs to tap external commercial borrowings

* Simultaneously, the government reduced withholding tax from 20% to 0%, significantly benefiting debt investors, who will now have access to a wider range of investible securities that were previously unavailable to them.

* The RBI and government measures are likely to garner close to USD75-80b in capital inflows in FY27. Further upside could materialize if India gets listed on a global bond index, which could lead to passive inflows of an additional USD15-20b, depending on India’s weight in the index.

* The implications for India’s balance of payments account and, consequently, the rupee outlook are substantial.

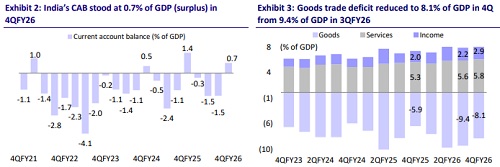

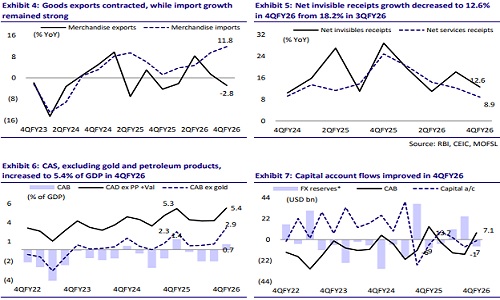

* Based on an assumed oil price of USD95pb in FY27, the capital account is now expected to post a surplus of USD80pb, compared to expectations of a deficit prior to the policy announcement. While the current account is still projected to remain above 2% of GDP or USD87b in FY27, the capital account is expected to offset most of this shortfall.

* India could now move close to a neutral BoP position in FY27 ((-)USD0.6b or 0.2% of GDP deficit). This materially changes the short-term outlook for the rupee.

* Assuming the Iran war is nearing its end, the rupee is likely to trade with an appreciation bias toward the 93 level over the next three to four months. Over the next 12 months, however, concerns around India’s twin deficits—the current and fiscal account deficits—and the continued strength of the US dollar are likely to resurface, exerting depreciation pressure on the rupee toward the 96 level, as against the earlier street expectation of 98-99.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412