The Credit-Deposit Ratio Moderates a Tad as both Credit Offtake and Deposit Growth Stumble - CareEdge Ratings

Synopsis

* Credit and deposit growth declined over the fortnight. The credit and deposit growth gap has narrowed to 0.08% from 0.78% in the previous fortnight. This is a significant change compared to the same period last year, when the gap was significantly larger at 5.71% (including merger impact).

* As of April 18, 2025, credit offtake reached Rs 181.9 lakh crore, marking an increase of 10.3% year-on-year (y-o-y), slower than last year’s rate of 15.3% (excluding merger impact). The slowdown can be attributed to a high base effect, muted growth across segments and typical behaviour at the beginning of the fiscal year.

* Deposits rose 10.2% y-o-y, totalling Rs 228.6 lakh crore as of April 18, 2025, a decrease from 13.3% the previous year (excluding merger impact). This slower growth is primarily attributed to a higher base effect and lower deposit interest rates.

* The Short-Term Weighted Average Call Rate (WACR) has decreased to 5.86% as of April 25, 2025, down from 6.92% on April 26, 2024. This decline follows two successive repo rate cuts by the Reserve Bank of India (RBI), bringing the WACR below the current repo rate of 6.00%.

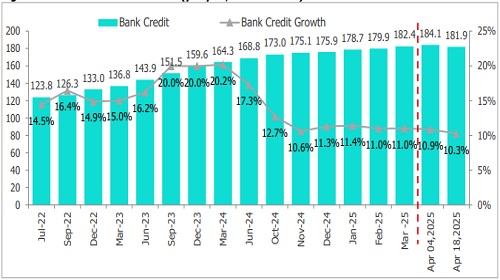

Bank Credit Offtake Declines for the Fortnight

Figure 1: Bank Credit Growth Trend (y-o-y %, Rs Lakh crore)

* Credit offtake rose by 10.3% y-o-y and declined by 1.2% sequentially for the fortnight ending April 18, 2025, yet it came in slower than the previous year’s growth of 15.3% (excluding the merger impact). This slowdown can be attributed to a higher base effect, RBI’s commentary on a high credit-to-deposit ratio, muted growth across segments and typical behaviour at the beginning of the fiscal year

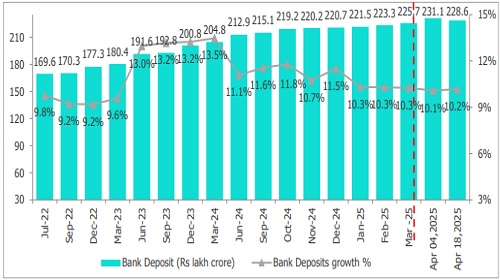

Figure 2: Bank Deposit Growth Witnesses a Marginal Uptick for the Fortnight (y-o-y %)

* Deposits increased by 10.2% y-o-y, reaching Rs 228.6 lakh crore as of April 18, 2025, lower than the 13.3% growth (excluding merger impact) recorded last year. According to the RBI, the issuance of certificates of deposit grew by 39.1% y-o-y to reach Rs 5.18 lakh crore as of April 18, 2025, as banks continued to rely on raising funds through certificates of deposit amidst subdued deposit growth. Further, during March 16 to April 16, 2025, the weighted average effective interest rate (WAEIR) of certificates of deposits stood at 6.69% and remained lower by 6 bps than the levels recorded a year ago.

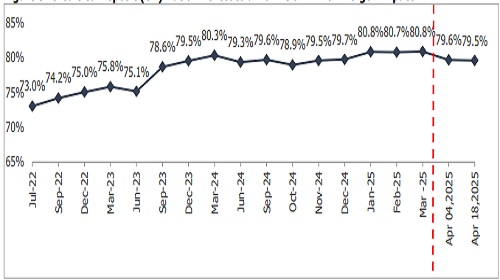

Figure 3: Credit-to-Deposit (CD) Ratio Witnesses a Downtick – Incl. Merger Impact

The Credit-Deposit (CD) ratio has experienced a marginal decline, slipping below the 80% mark for the second time in the past three months. The CD ratio decreased by 10 basis points over the previous fortnight, reaching 79.5% as of April 18, 2025.

The Proportion of Bank Credit Declines while the government invests. to Total Assets Witness an Uptick

Figure 4: Proportion of Govt. Investment and Bank Credit to Total Assets (%)

* The credit-to-total-assets ratio decreased marginally to 69.3%, while the Government Investment-to-totalassets ratio witnessed a minor uptick at 25.5% for the fortnight ending 04 April 2025. Meanwhile, overall government investments totalled Rs 66.9 lakh crore as of April 18, 2025, reflecting a y-o-y growth of 8.8% and a sequential increase of 0.4%.

Above views are of the author and not of the website kindly read disclaimer

.jpg)

.jpg)