India`s API Industry Expected to Grow at a CAGR of 5-7% till FY28 by CareEdge Ratings

Synopsis

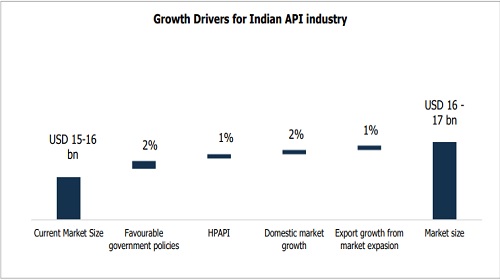

* The Indian Active Pharmaceutical Ingredient (API) market, currently valued at approximately USD 15-16 billion, is projected to grow at a CAGR of 5–7% in FY27 & FY28. The growth trajectory is supported by favourable government policies, a structural shift towards high-potency (HP API) and complex APIs, steadily rising domestic demand, and greater penetration into regulated and emerging markets.

* Pharma firms are shifting from basic APIs to complex APIs—aiming to counter price erosion, strengthen margins, and customer retention. Import reliance on China for Key Starting Materials (KSMs) remains high, though government initiatives are beginning to show progress.

* Indian API manufacturers are modernising production by integrating sustainability, technology, and efficiency through Artificial Intelligence (AI), data analytics, and flow manufacturing.

India’s API Industry: Setting the Stage for Growth

India’s API industry, with a market size of USD 15-16 billion, is entering a period of steady expansion. Over the next two years, growth of 5–7% is expected, supported by factors such as an ageing population, wider healthcare access, rising insurance penetration, and the increasing prevalence of chronic diseases. The industry is also being shaped by opportunities resulting from the loss of exclusivity on several drugs and by expansion into emerging markets. At the same time, a pipeline of high-potent and complex APIs are being developed, with commercialisation expected in the coming years, pointing to India’s gradual move up the value chain. Technology adoption and modern manufacturing practices are beginning to play a role as well, setting the stage for how competitiveness and efficiency will evolve across the sector.

Where it Begins: Basics of the API Industry

An example of the manufacturing process and costs involved

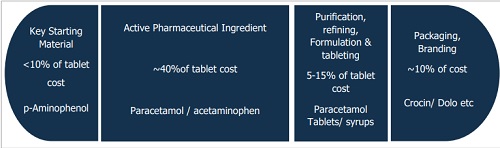

Medicine manufacturing involves 8-10 stages, with key starting materials (KSMs), active pharmaceutical ingredients (APIs), and formulations as critical components. KSMs are the primary raw materials, while APIs are the active substances that make the medicines effective. KSMs undergo multiple chemical and physical processes to produce APIs, which are then combined with inactive components (excipients) to produce finished drug forms (FDF)/ formulations. This is then packaged with branding and sold. For example, p-Aminophenol is one of the KSM, acetaminophen (paracetamol) is the API, and the final formulation is marketed under different brands.

KSMs are generally produced in bulk and are subject to lesser regulation than APIs, making them cheaper due to economies of scale and relatively lower compliance costs. However, they are vital for supply chain stability and uninterrupted API production. Most value addition occurs at the API and finished drug stages, which are highly regulated and central to the pharmaceutical value chain.

Indian pharmaceutical companies are steadily transitioning from pure API manufacturing to more complex and specialised areas such as High Potent APIs (HPAPIs), contract development and manufacturing (CDMO), and formulations. While solely API-focused players currently face increased competition, this transition is expected to strengthen long-term pricing power, improve margins, enhance compliance, and increase customer retention.

Key Forces Reshaping the Indian API Industry

The Indian API industry is entering a phase of structural change driven by both domestic imperatives and global market dynamics. Rising regulatory scrutiny, evolving customer expectations, and the need for technological sophistication are reshaping how companies operate. At the same time, competitive pressures and supply chain vulnerabilities are compelling companies to rethink their strategies, moving beyond volume-driven growth towards specialisation and value creation. These forces are not isolated; they interact to define the industry’s trajectory and will determine how Indian manufacturers position themselves in the global pharmaceutical ecosystem.

Above views are of the author and not of the website kindly read disclaimer