Sell Tata Elxsi Ltd for Target Rs.4,700 by Choice Institutional Equities

Improving Earnings Visibility, But Risk-reward Remains Unfavorable

TELX reported modest revenue growth, indicating clear sign of operational stability. While near-term demand headwinds persist in Media & Communications and parts of Healthcare, growth visibility has improved, led by strong Transportation momentum from SDV-led OEM ramp-ups, client normalisation and expanding adjacency opportunities. Margin rebounded sharply on operating leverage, improved utilization and cost discipline, despite wage hikes. While fundamentals are improving, we believe much of the medium-term recovery is priced in. We maintain our PE multiple at 28x, arriving at a TP of INR 4,700 based on average FY27E–FY28E EPS. We reiterate our SELL rating, while noting that sustained double-digit growth momentum in the Transportation & HLS vertical and margin normalisation could act as potential re-rating triggers.

Revenue in line; EBITM Ahead of Estimate; PAT Impacted by One-offs

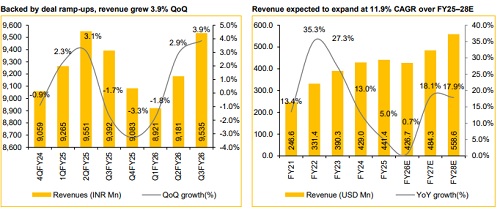

* Revenue for Q3FY26 came in at INR 9.5Bn, up 3.2% QoQ but down 5.5% YoY in CC. In INR terms, revenue rose 3.9% QoQ and 1.5% YoY (vs CIE est. at INR 9.6Bn).

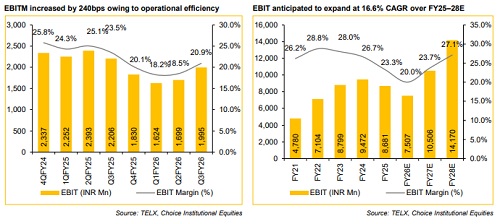

* EBIT for Q3FY26 came in at INR 1.9Bn, up 17.4% QoQ but down 9.6% YoY (vs CIE est. at INR 1.8Bn). EBIT margin was up 240bps QoQ but down 260bps YoY to 20.9% (vs CIE est. at 19.7%).

* PAT for Q3FY26 stood at INR 1.1Bn, down 29.6% QoQ and 45.2% YoY (vs CIE est. at INR 1.7Bn).

Steady Quarter; Revenue Growth Driven by Transportation & HLS: TELX delivered a steady 3QFY26 with 3.2% QoQ CC revenue growth, driven by volume-led execution and improved utilization. Transportation led growth (+7.7% QoQ) led by SDV deal ramp-ups, client normalisation and early traction in off-road and adjacency businesses. Media & Communications was marginally soft (-0.3% QoQ) due to seasonality, while Healthcare & Life Sciences appears to have bottomed out, with GenAI-led wins expected to support recovery from 4QFY26. We believe near-term growth remains stable, with gradual improvement from Q4FY26 driven by continued Transportation deal ramp-ups large-deal ramp-ups and improvement in utilization, while recovery in Media and HLS should provide incremental support.

Sequential Margin Recovery, Utilization Levers to Drive FY27E Growth: EBITM expanded sharply by 240bps QoQ to 20.9%, driven by operating leverage from higher utilization, disciplined cost control and a modest FX tailwind, partly offset by wage hike. Management indicated 200bps benefit from operating leverage and 80–85bps from cost control, offset by a 110bps margin impact from junior-to-mid staff wage revision. Utilization stands at 75%, with a target of 80% before capacity addition. Hiring remains selective, with large-scale additions deferred by a couple of quarters. We expect FY26 EBITM to stabilise at 20.0%, with a return to the 23–24% band in FY27E, dependent on sustained revenue growth and operational execution. We maintain a constructive medium-term view, given the company’s strong cost discipline, improving utilization trajectory and leverage potential from large deal ramp-ups in Transportation and Healthcare.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

600-400.jpg)