Reduce KNR Constructions Ltd For Target Rs. 165 By JM Financial Services

Challenging times ahead

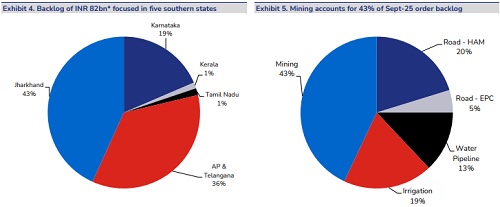

KNR Constructions reported dismal earnings in 2Q26 as adjusted PAT slumped 70% YoY to INR 279mn (JMFe: INR 400mn, consensus: INR 539mn) due to lower margins/other income. Irrigation receivables from Telangana government inched up further to INR 13.5bn. With strong inflows of INR 40bn in 1H26, backlog improved to INR 82bn (3.2x TTM revenue) as of Sept-25. However, only 43% of backlog is currently under execution. Also, EBITDA margins have been impacted due to operating deleverage, lower share of high margin irrigation segment and cost incurred towards Kerala project on KNR’s books. Due to softer execution in 1H26 and weak executable backlog, KNR has further lowered its FY26E revenue guidance to c.INR 20bn (from INR 20–25bn earlier). Margins in 2H26 will be further impacted by cost of c.INR 400mn to be incurred in Kerala project. Accordingly, we have cut EPS sharply by 45%/25%/12% in FY26/27/28E led by cut in execution/margins. Valuations at 18x/13x FY27/28E EPS does not provide material upside. We downgrade the stock to REDUCE with SoTP based revised price target of INR 165 (valuing EPC business at 13x FY27 EPS and assets at INR 45/share).

* PAT sharply below JMFe due to lower margins and other income: KNR’s revenue/EBITDA declined sharply by 42%/61% YoY to INR 4.9bn/INR 536mn (JMFe: INR 4.3bn/INR 574mn) due to lower executable order backlog. Irrigation revenue stood at c.INR 1.7bn (+17% YoY), above JMFe of INR 1bn. EBITDA margins contracted sharply by 520bps YoY to 10.9% (JMFe: 13.5%) due to higher employee expenses (includes c.INR 100mn variable payout to promoters) and INR 100mn cost incurred towards Kerala project (on KNR’s books). Other income declined sharply by 73% YoY to INR 39mn (JMFe: INR 160mn). Adjusted PAT declined sharply by 70% YoY to INR 279mn (JMFe: INR 400mn) due to lower margins and other income.

* Backlog strengthens but executability weak; cuts FY26E revenue guidance sharply: With strong inflows of INR 40bn in 1H26, KNR’s order backlog has improved to INR 82bn (3.2x TTM revenue) as of Sept-25. However, execution of the recently awarded INR 36bn mining order has been deferred by 9–12 months, with meaningful revenue contribution now expected in FY28E. Due to softer execution in 1H26 and weak executable backlog, KNR has further lowered its FY26E revenue guidance to c.INR 20bn (from INR 20–25bn earlier). Margins in 2H26 will be further impacted by cost of c.INR 400mn to be incurred in Kerala project and we estimate it to be around 10-11% in 2H26. KNR expects order inflows of INR 120-140bn for FY26E.

* Irrigation receivables rose further; asset monetization in sight: Irrigation receivables from Telangana government rose further from INR 13bn in Aug-25 to INR 13.5bn currently. KNR received c.INR 744mn in 3Q26 so far and is hopeful of improved recoveries in 2H26. KNR has a pending equity requirement of INR 2.9bn for its HAM portfolio, to be infused in FY26/27E. KNR targets to complete monetization of 4 HAM assets in 2H26.

* Downgrade to REDUCE with price target of INR 165: While KNR derives intrinsic strengths from a proven track record, good governance and strong balance sheet we see uncertainties in its medium growth outlook caused by uncertain prospects for its irrigation segment weak executable backlog. We have cut EPS sharply by 45%/25%/12% in FY26/27/28E mainly led by cut in execution and margins. Valuations at 18x/13x FY27/28E EPS does not provide material upside. We downgrade the stock to REDUCE with SoTP based revised price target of INR 165 (valuing EPC business at 13x FY27 EPS and assets at INR 45/share).

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361