Neutral Westlife Foodworld Ltd For Target Rs. 800 by Motilal Oswal Financial Services Ltd

Focus on volume growth; store expansion continues

* We recently hosted Westlife Foodworld’s (WESTLIFE) management at our Ideation Conference to gain insights into the company's current business environment and future plans. Over the past six months, the company has experienced a stable demand environment, with a slight improvement in 4QFY25, however this is seasonally weak quarter. A favorable base is further contributing to an improved growth print. Consumer sentiment is expected to pick up gradually from late 1QFY26, driven by potential interest rate cuts and fiscal measures implemented in Budget 2025. Regionally, recovery remains stronger in the west, while the south, particularly Kerala and Hyderabad, is witnessing a gradual improvement. The company continues to focus on menu innovation and value-oriented offerings to attract customers. It is strengthening its fried chicken portfolio in South India, aligning with local consumer preferences. Store expansion remains a key focus, with plans to open 45 new stores in FY25 and a target of 580-600 stores by Dec’27. As of Dec’24, the company opened 25 stores YTD, bringing the total count to 421, with drive-thrus accounting for 22% (93 restaurants). McCafé is emerging as a key growth driver, contributing 12-13% to Average Daily Sales (ADS). It has the potential to reach 18-20%, benefiting from McDonald's existing infrastructure. WESTLIFE continues to enhance its omnichannel presence, with off-premise sales contributing 40-42%. Additionally, the company is running pilots for a 10-minute delivery model, primarily focused on beverages.

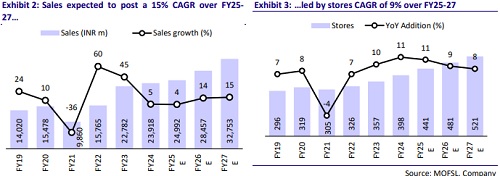

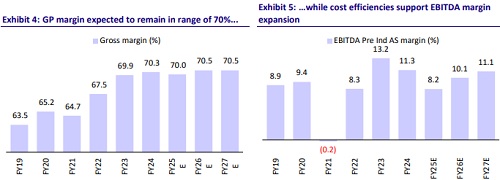

* Despite inflationary pressures, WESTLIFE has successfully maintained gross margins at ~ 70%, supported by efficient supply chain management, cost control initiatives, and selective price hikes at the portfolio level. The company follows a strategic pricing approach, typically implementing modest price hikes of 2-4% to offset around 50% of its inflationary impact while maintaining market competitiveness. The company is prioritizing margin expansion through cost control initiatives, which are expected to yield benefits over the next two to three quarters. However, volume growth will remain the primary driver for margin expansion. The company targets an EBITDA margin of 18-20%, with a pre-Ind AS EBITDA margin goal of 14-15%. Same-store sales growth (SSSG) in the mid-single digits is expected to support higher ADS. We model 14-15% revenue CAGR for FY25-27, driven by 9% store additions and 6-7% SSSG. We expect 10-11% EBITDA Pre Ind AS margin for FY26 and FY27.

* We have recently upgraded our view on the QSR universe from cautious to positive following the tax relief announced in Budget 2025 for the middle-class income group. We remain watchful for ADS recovery as it could swiftly improve unit economics. We reiterate our Neutral rating on the stock with a TP of INR800, based on 35x FY27E EV/EBITDA (pre-IND-AS).

Stable near-term demand

Westlife Development has experienced a stable demand environment over the past six months, with slight improvement in 4QFY25. Despite the seasonal softness in 4Q, underlying consumer demand remains resilient. Management expects traction to improve by late 1QFY26 and early 2QFY26, supported by potential interest rate cuts by the RBI and fiscal measures from Budget 2025, such as tax reliefs aimed at boosting consumption. Consumer sentiment remains a key driver, particularly in small-ticket transactions, where positive sentiment translates into higher discretionary spending. Regionally, recovery has been more pronounced in the western market, while southern markets like Kerala and Hyderabad are recovering at a slower pace. The company remains committed to long-term investments in these regions to drive sustainable growth.

Strengthening the chicken portfolio in South India

WESTLIFE is strategically strengthening its presence in the fried chicken category, particularly in southern markets, where chicken consumption trends align with local preferences. To drive this initiative, the company has appointed a dedicated team with expertise in the chicken portfolio. As part of this strategy, WESTLIFE is introducing a new product range tailored to regional tastes, focusing initially on the southern market. While McDonald's has a strong global presence in the chicken segment, its approach in India is region-specific. In the western region, chicken preferences lean towards boneless formats, leading to the launch of McCrispy Chicken Burgers. However, given the predominantly vegetarian population in the west, the company does not plan to introduce a full-fledged chicken portfolio in that market

Store expansion continues

WESTLIFE remains committed to expanding its store network, targeting 45 new store openings in FY25. As of Dec’24, the company opened 25 stores YTD, bringing the total count to 421, with drive-thrus accounting for 22% (93 restaurants). By Dec’27, the company aims to expand its footprint to 580-600 stores, with a strategic focus on South India, smaller towns, and drive-thrus. Unlike peers, WESTLIFE follows a distinct real estate strategy based on ROI-driven site selection, securing long-term lease agreements of 20-25 years with periodic renewals in three to five years to adjust for inflation.

McCafé serves as a key growth driver

India’s café segment continues to experience rapid growth, driven by favorable demographics and evolving consumer preferences toward social dining. McCafé is positioned as a critical growth driver for WESTLIFE, currently contributing 12-13% to ADS, with the potential to reach 18-20%, while also being margin accretive. Unlike standalone coffee chains, which often struggle with profitability, McCafé leverages McDonald’s existing infrastructure, making it a highly profitable segment. As of Dec’24, McCafé was present in 401 restaurants, covering 95% of the total 421 stores.

Continues to leverage omnichannel strategy

Globally, on-premise and takeaway channels account for the majority of sales, with delivery contributing 20-30%. For WESTLIFE, the channel mix is expected to remain stable in the medium term, with off-premise sales maintaining a 40-42% share. The company continues to leverage its omnichannel proposition, presence across multiple dayparts, and multi-brand offerings, which serve as key drivers of AUV growth. To further enhance the delivery experience, the company is piloting a 10- minute delivery model in select restaurants. A few QSR players are capable of executing rapid-turnaround delivery models, and WESTLIFE’s well-integrated network positions it well to effectively capitalize on this opportunity, particularly in the beverages segment.

Focus on margin expansion

Despite inflationary pressures on food and utilities, WESTLIFE has successfully maintained gross margins above 70%, supported by supply chain efficiencies, cost initiatives, and selective price hikes at the portfolio level. The company follows a pricing strategy of implementing small annual price hikes of 2-4% to offset inflation, aiming to pass on at least 50% of inflationary costs while remaining competitive. The company continues to focus on margin expansion through robust cost control programs, with benefits expected to materialize over the next two to three quarters. Volume growth is anticipated to play a key role in margin expansion. The company is targeting an EBITDA margin of 18-20%, with a pre-Ind AS EBITDA margin of 14-15%. SSSG in mid-single digits is expected to support improvements in ADS. The company remains focused on increasing its market share and optimizing operational efficiencies. It aims to achieve sustainable growth by strategically increasing guest traffic and driving volume-led expansion, rather than relying heavily on price adjustments.

Valuation and view

* We believe that once the demand environment improves, WESTLIFE will be a key beneficiary. The company has been more aggressive in-store additions, which was not the case historically. The current demand environment is not conducive to aggressive expansion; therefore, the benefits of these efforts are likely to be back-ended.

* The revenue gap between dine-in and delivery has narrowed, driven by improved dine-in footfall. We remain watchful for ADS recovery, as it could quickly enhance unit economics. The stock is currently trading at ~38x FY26E and ~29x FY27E pre IND-AS EBITDA. We reiterate our Neutral rating with a TP of INR800, based on 35x FY27E EV/EBITDA (pre-IND-AS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412