Neutral United Spirits Ltd For Target Rs. 1,500 by Motilal Oswal Financial Services Ltd

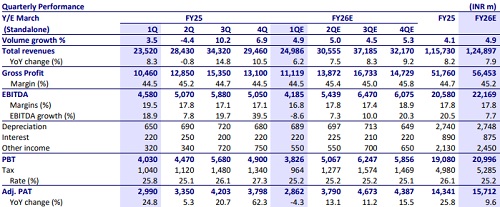

* The P&A segment’s volume growth remained subdued in 1QFY26, partly due to a high base in 1QFY25, which had benefited from election-related inventory stocking. We model 5% volume growth and 7% revenue growth in the P&A segment.

* We model 5% volume growth and 8% revenue growth in the popular segment.

* Gross margins are expected to remain stable at 44.5%, given the stabilization in input prices. EBITDA margin is expected to contract 270bp YoY, impacted by elevated expenses and some degree of operating deleverage during the quarter.

* The impact of Maharashtra’s import duty changes, primarily affecting the lower- to mid-prestige segments, will be more visible in 2QFY26. However, the upper prestige segment remains largely unaffected.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...