Neutral KFin Technologies Ltd for the Target Rs.1000 by Motilal Oswal Financial Services Ltd

* KFin Technologies’ (KFin) revenue grew 23% YoY—Ascent business added from 3QFY26—but declined 6% QoQ to INR3.5b in 4QFY26 (5% miss led by a miss on MF and issuer solutions business). For FY26, revenue grew 21% YoY to INR13.2b.

* Total opex grew 36% YoY/remained flat QoQ to INR2.2b (in line), with employee expenses/other expenses up 49% YoY to INR1.5b (includes INR40m impact of labor code)/14% YoY to INR671m. EBITDA grew 5% YoY but declined 15% QoQ to INR1.3b, with EBITDA margins at 37% vs 43.2% in 4QFY25 (MOFSLe of 40.2%).

* KFin reported a net profit of INR811m, down 5% YoY/12% QoQ (13% miss - mainly due to a miss on the topline) in 4QFY26, with PAT margin at 23.4% vs 30.1% in 4QFY25. Excluding the impact of labor code of ~INR40m, there was a 9% miss on PAT. For FY26, KFin reported a PAT of INR3.7b, rising 10% YoY.

* FY27 guidance implies revenue/EBITDA/PAT growth of ~23–25% /~16–17% (margins ~39–40%)/~10%, assuming no meaningful improvement in the asset mix—leaving room for upside if markets recover. On an organic basis, revenue/EBITDA are expected to grow at ~15%/~11%, respectively.

* We have cut our earnings estimates by 11% each for FY27/FY28. While revenue estimates were largely unchanged (lower MF income offset by higher international revenues), higher depreciation pertaining to the new office led to earnings cut. We expect KFin’s revenue/EBITDA/PAT to expand at a CAGR of 20%/19%/16%, respectively, over FY26–28. We reiterate a Neutral rating on the stock, with a one-year TP of INR 1,000, based on a 36x FY28 EPS multiple.

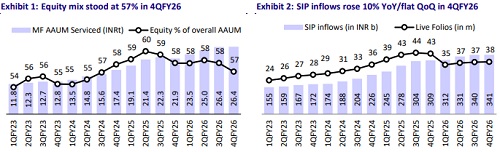

Equity AAUM share declines sequentially

* KFin’s total MF AAUM serviced during the quarter rose 21% YoY/remained flat QoQ to INR26.4t. Equity AAUM, at 56.7% of total MF AAUM, grew 18% YoY/declined 2% QoQ to ~INR15t, reflecting a market share of 32.1% (33.1% in 4QFY25).

* Equity AUM share has declined over the past two quarters due to higher passive (notably commodity ETFs) allocation and lower hybrid exposure, though early Apr’26 trends indicate a reversal toward active equity flows.

* MF revenue grew 8% YoY but declined 4% QoQ to INR2.2b (~62% mix) despite a 21% YoY AAUM growth, driven by pricing cuts (Apr’25), shift toward lower-yield passive mix, and MTM-led realization impact.

* MF yields declined to 3.3bp in 4QFY26 from 3.6bp in 4QFY25 and 3.4bp in 3QFY26 due to an increasing share of low-yielding passive mix trend, which is expected to improve.

* On the MF side, the company won two new SIF mandates and a contract from an AMC for developing digital assets under the MF segment.

* In issuer services, revenue declined 16% YoY/35% QoQ to INR356m, due to: 1) folio erosion; 2) weak corporate actions in 4Q due to global uncertainty; and 3) base effect (one-off event last year - 4QFY25 had a large demerger transaction, which boosted revenue).

* The mainboard IPO market share (issue size basis) rose sequentially to 58.3% in 4QFY26 from 43.4% in 3QFY26 despite a fall in the number of IPOs handled (9 vs 11 in 3QFY25).

* In international investor solutions, revenue (ex-Ascent) grew 17% YoY/3% QoQ to INR441.8m; including Ascent, revenue surged 143% YoY/114% QoQ, raising segment contribution to 16.7% (vs 3.8% in 3QFY25; 4.6% in 2QFY26). The company has guided for revenue growth at ~70%+ YoY (~60%+ organic growth) for FY27.

* In the alternates and wealth business, KFin’s AUM grew ~19% YoY but declined by 6% QoQ due to MTM pressures, led by equity market corrections. Its market share stood at 38.1% vs 36.8% in 4QFY25.

* The NPS business saw strong outperformance with ~36% subscriber growth vs ~12% industry, driven by tech-led initiatives and new offerings (e.g., gig pension, health-linked withdrawals); shift to bps-based pricing enhances scalability, with market share rising to 11.9% (from 9.8% YoY).

* Non-domestic MF revenue contribution rose to ~38% (vs 30% YoY), with management guiding for >50% in the medium term, while value-added services share moderated to ~6% from 7% in 4QFY25/6.8% in 3QFY26.

* Total operating expenses grew 36% YoY/remained flat QoQ to INR2.2b (in line), with employee expenses growing 49% YoY to INR1.5b (includes one-time INR40m impact of labor code) and other expenses growing 14% YoY to INR671m. The cost-to-income ratio was at 63% (56.8% in 4QFY25).

* Other income rose 50% YoY/126% QoQ to INR150m (vs our estimates at INR27m).

Key takeaways from the management commentary

* The company plans to reduce domestic MF mix to below 50% from ~62% currently over the medium term. Its focus will remain on expanding the international business; high-growth segments like AIF and pension; and technology-led value-added services.

* Under the international business, the company successfully completed the POC stage for the platform deal from one of the largest banks in the Philippines, with project development expected to kickstart in 1QFY27.

* Management expects the client addition momentum to accelerate further for the international business as global markets stabilize; growth could exceed current quarterly additions (~60+ clients per quarter) over time.

Valuation and view

* Structural tailwinds in the MF industry are expected to drive absolute growth in KFin’s MF revenue. With its differentiated ‘platform-as-a-service’ model offering, technology-driven, asset-light model, increasing contribution from non-MF segments, and integration of global fund administration capabilities through Ascent, KFin is well-positioned to capitalize on strong growth opportunities in both Indian and global markets.

* We have cut our earnings estimates by 11% each for FY27/FY28. While revenue estimates were largely unchanged (lower MF income offset by higher international revenues), higher depreciation pertaining to the new office led to earnings cut. We expect KFin’s revenue/EBITDA/PAT to expand at a CAGR of 20%/19%/16%, respectively, over FY26–28. We maintain a Neutral rating on the stock, with a one-year TP of INR 1,000, based on a 36x FY28 EPS multiple.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041