Neutral Eicher Motors Ltd for the Target Rs.6,960 by Motilal Oswal Financial Services Ltd

Domestic demand sustains; export outlook uncertain

We met with Eicher Motors (EIM)’s management to gain insight into the business outlook amid the challenging global macroeconomic environment. Domestic demand momentum remains healthy, especially in the 350cc segment, where demand currently outstrips supply. Conversely, demand in the 350cc+ segment weakened following the GST increase for this category, but is now gradually recovering due to multiple product interventions by RE. However, the export outlook remains a mixed bag as the outlook for regions such as Europe, the US, and Thailand – which account for half of EIM’s exports – remains challenging, while the outlook for the other half remains positive. The immediate risk posed by the ongoing geopolitical conflict is a potential gas supply shortage, which could disrupt production in the near term if the situation persists. Management emphasized its continued focus on profitable volume growth rather than margins. Owing to the global uncertainties, the stock has corrected about 17% from its peak and now appears fairly valued at 29.8x FY27E and at 26.0x FY28E. We upgrade the stock to Neutral with a revised TP of INR6,960. We value RE at 28x Dec’27E EPS and VECV at 12x EV EBITDA.

Domestic demand remains upbeat in the 350cc segment

The GST rate cuts have helped RE sustain its demand momentum, especially in the 350cc segment, where demand currently exceeds supply and booking growth continues to outpace wholesale growth. In the 350cc+ segment, demand is relatively weak due to the rise in GST rates. However, given the supply constraints – especially for the 350cc models – RE is in the midst of a capacity expansion that will gradually increase its capacity from the current 1.2m units to 2m units p.a. by FY28, with an investment of about INR9.6b. While the two-wheeler industry growth outlook is expected to be in the high single digits for FY27E, RE aims to outperform the industry growth.

Modest export outlook

About 50% of RE’s export regions are facing demand headwinds, including Europe (due to the macro slowdown), North America (because of high tariffs), and Thailand. Conversely, other regions continue to demonstrate healthy growth, which include Brazil (a key growth driver), other LATAM regions such as Argentina and Colombia, as well as APAC regions such as Japan, Australia, NZ, and South Korea. In the near term, RE will focus on these growth regions while aiming to maintain volumes in the regions facing challenges.

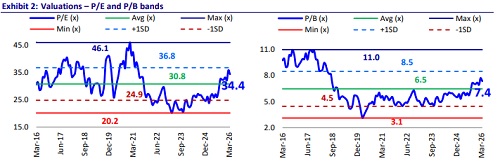

Valuation and view

We project EIM to achieve a CAGR of 18%/17%/15% in revenue/EBITDA/PAT over FY25-28E. Amid global uncertainties, the stock has corrected about 17% from its peak and now appears fairly valued at 29.8x FY27E and 26.0x FY28E. We upgrade the stock to Neutral with a revised TP of INR6,960. We value RE at 28x Dec’27E EPS and VECV at 12x EV EBITDA.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041