Neutral Exide Ltd for the Target Rs. 327 by Motilal Oswal Financial Services Ltd

Exports and telecom drag down revenue growth

Surge in input costs to hurt margins in the near term

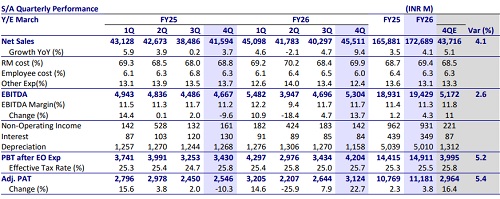

* Exide’s 4QFY26 PAT at INR3.1b came in slightly above our estimate of INR3b. Most key segments reported healthy double-digit growth YoY. However, revenue inched up only 9.4% mainly due to weak exports and a continued decline in the telecom segment.

* The outlook for lead-acid business remains positive for the auto segment and the industrial business (excl. telecom). However, we remain cautious about the long-term returns from the lithium-ion business. Besides, the stock trading at ~26.1x/23.3x FY27E/28E EPS appears fairly valued. Reiterate Neutral with an SoTP-based TP of INR327. We value the core (lead acid) business at 15x FY28E EPS (in line with Amara). We add INR59 per share value for the EV business (based on book) and INR50 per share for its stake in HDFC Life.

Margins in line; PAT slightly ahead of estimates

* EXID’s 4QFY26 revenue came in line with our estimate, growing 9.4% YoY to INR45.5b. Overall, domestic business grew 12.5% YoY, despite a 50% drop in telecom. Exports continued to show a double-digit dip due to notable headwinds, led by the ongoing geopolitical crisis, unavailability of containers, and disruption in shipping routes.

* Auto OEM business grew 25%+ YoY, leading to increased market share across multiple segments. 2W/4W replacement business posted doubledigit growth on a YoY basis.

* The industrial infra business (ex-telecom) also clocked double-digit growth as order inflow and order execution picked up in sectors like railways, traction, etc. Inverters and solar business are back on a growth trajectory, posting mid-to-high teen growth on a YoY basis, buoyed by peak season demand in the second half of 4Q.

* EBITDA margin came in at 11.7%, in line with our estimate. Despite sharp INR depreciation, EXID was able to increase margins by 40bp YoY due to an improved product mix and better realization, aided by lowering warranty costs. EBITDA also came in line, growing 13.7% YoY to INR5.3b.

* PAT came in slightly above estimates at INR3.1b, up 22.7% YoY.

* For FY26, EXID’s revenue/EBITDA/PAT rose 4.1%/4.3%/3.8% to INR173b/ INR19.4b/INR11.2b. CFO stood at INR22.3b, while FCF was INR18.2b. The company continues to be debt-free despite high capex.

* The board has recommended a dividend of INR2 per equity share for FY26, the same as last year.

Highlights from management call

* Management remains constructive on the outlook of its core lead-acid business, expecting high single-digit to low double-digit growth potential in the near term and indicating that medium-term growth could broadly remain in line with the company’s historical ~11% CAGR.

* Rising input costs are likely to hurt margins in the near term. Costs of key inputs like sulphur and plastics have spiked in the recent past. For instance, sulphur prices have gone up from ~INR15 one year back to ~INR75 at Apr’26 end (stood at INR58 as of Mar’26 end).

* To mitigate input cost inflation, the company has implemented multiple price hikes in the replacement segment in 4Q, amounting to a total of 5-6%, followed by an additional ~3% hike in April. Even these price hikes do not cover for the entire input cost inflation currently, with management indicating further possible hikes in 1QFY27.

* Exide Energy Solutions invested INR6b in 4Q and INR15b in FY26, taking the cumulative infusion to ~INR48b, with an additional INR14b earmarked for FY27 for capex and working capital requirements for Phase 1 ramp-up.

Valuation and view

The outlook for lead-acid business remains positive for the auto segment and the industrial business (excl. telecom). However, we remain cautious about the longterm returns from the lithium-ion business. Besides, the stock trading at ~26.1x/23.3x FY27/28E EPS appears fairly valued. Reiterate Neutral with an SoTPbased TP of INR327. We value the core (lead-acid) business at 15x FY28E EPS (in line with Amara). We add INR59 per share value for the EV business (based on book) and INR50 per share for its stake in HDFC Life.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412