Neutral Blue Star Ltd for the Target Rs.1,950 by Motilal Oswal Financial Services Ltd

Swift reset and growth optimism largely priced in

Demand tailwinds and margin expansion to drive earnings growth

* Blue Star (BLSTR)’s stock rallied over 25% in the last two weeks from its recent low due to an improving demand outlook with rising temperatures across regions, following unseasonal rains at the end of Mar’26. A return to typical seasonal conditions, accompanied by the onset of heat in southern and western regions from mid-Apr’26, is likely to drive a sharp recovery in room air conditioner (RAC) demand. The company is operationally well-prepared for this trend change, with available channel inventory, an expanded portfolio of 125 BEE-compliant models, and calibrated price hikes to protect margin.

* From a medium-to-long-term perspective, the company is entering into a favorable phase marked by improving competitive positioning, benefits from backward integration, and a robust, diversified order book across infrastructure, commercial real estate, and data centers. It has strategically focused on high-margin verticals like factories, data centers, hospitals, and organized retail, driving faster execution and better client quality. Management’s consistent focus on execution discipline and capital allocation further reinforces earnings visibility and return ratios.

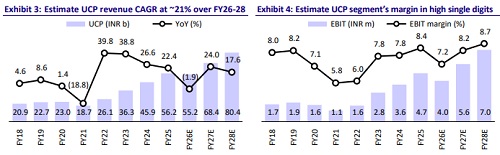

* We raise our EBITDA estimates by ~5% each for FY27 and FY28. We forecast a CAGR of ~17%/24%/32% in revenue/EBITDA/PAT over FY26-28, fueled by healthy growth across UCP and MEP & CAC businesses. We estimate OPM to expand ~50bp/30bp in FY27E/FY28E, led by positive operating leverage and cost-saving initiatives.

* At CMP, BLSTR trades fairly at a P/E of 54x/43x on FY27/FY28E. Our SoTP-based TP stands at INR1,950 (valuing UCP/EMPS at 45x each and PES at 25x FY28E EPS). Reiterate Neutral.

Backward integration driving margin expansion

* BLSTR’s margin expansion strategy is anchored in backward integration and accelerating the indigenization of key RAC components. The Sri City facility has been rapidly scaled up and is expected to further expand capacity by FY27E, supported by high automation and digitized processes that enhance cost control and supply chain reliability. The company is also localizing critical functions to improve cost efficiencies and reduce import dependence.

* The company maintains strong leadership in commercial refrigeration with dominant market shares across deep freezers and modular cold rooms. Key structural drivers are the formalization of India’s food supply chain through the expansion of cold chain infrastructure under government-led postharvest initiatives and the steady rise of organized food retail.

* Overall, a richer product mix, a higher share of inverter ACs, disciplined pricing, and backward integration have enabled BLSTR to consistently outperform its peers in terms of margins, while steadily gaining market share in the RAC segment.

RAC: Weathering short-term headwinds; structural growth story strong

* The Indian RAC industry is facing near-term headwinds from erratic weather, GST-led demand deferment, regulatory changes (BEE revisions), and inflationdriven price hikes, impacting affordability and sales conversion. These factors have led to uneven primary-to-secondary offtake and rising channel inventory, with demand remaining highly weather-sensitive.

* However, the long-term outlook remains structurally strong, supported by low penetration (~12–14% vs. ~42% globally), improving affordability, and rising income levels. As electrification deepens, the addressable market is expanding, with ~150m households expected to become AC-affordable over time.

* Industry volumes are projected to grow from ~13m units in FY26 to ~23m units by FY30 (~15-16% CAGR). In value terms, the market is estimated to clock ~18- 19% CAGR over FY26-30 to reach INR540b. Urbanization, premiumization, and strong demand from Tier 3-5 markets will fuel growth, alongside increasing replacement demand as the installed base matures.

* It has launched an expanded RAC portfolio for summer 2026 with 125 models. The range spans premium offerings such as Iconia, heavy-duty, hot & cold, and anti-virus ACs, targeting diverse consumer segments and use cases. The premium push is further supported by tightening BEE efficiency norms, which are reducing entry-level differentiation and shifting value creation toward advanced features and brand positioning, where BLSTR is well placed, given its strong HVAC engineering capabilities.

EMPS & CAC: Growing data center exposure and disciplined execution

* The EMPS and CAC segment is well-positioned to benefit from India’s ongoing capex upcycle, backed by a strong and diversified order book across commercial real estate, infrastructure, data centers, and industrial projects, ensuring healthy medium-term revenue visibility. As execution scales up, operating leverage is expected to drive margin expansion through better absorption of fixed costs. It has strategically focused on high-quality verticals such as factories, data centers, hospitals, and organized retail, which offer superior margins, faster execution, and stronger counterparties. It also maintains a leadership position across key HVAC categories, strengthening its competitive positioning.

* Data centers are emerging as a key structural growth driver, with India’s capacity expected to expand sharply by 2030, driven by data localization, cloud adoption, and AI-led investments. This presents a multi-year opportunity, supported by significant capex commitments from global and domestic players. The segment offers high-margin, engineering-intensive opportunities in precision cooling and MEP systems, where the company has strong capabilities, creating entry barriers and enabling better pricing discipline.

* India’s data center capacity is expected to scale sharply from ~1.5 GW currently to ~5.0 GW by 2030. Data center construction cost is estimated at USD5.6-8.6m/ MW. Out of this, MEP spending (including cooling, fire suppression, and life safety systems) is estimated at ~USD2.2–3.4m/MW (~40% of data center cost). The projected capacity addition by FY30E implies a USD7.8-12.0b addressable MEP market over the next four years. BLSTR, leveraging its established presence in commercial HVAC and proven MEP execution capabilities, is well-positioned to participate meaningfully in the HVAC and electromechanical opportunities arising from this data center build-out.

Valuation and view

* We estimate a CAGR of ~17%/24%/32% in revenue/EBITDA/PAT over FY26-28, fueled by healthy growth across UCP and MEP & CAC businesses. We estimate OPM to expand ~50bp/30bp YoY in FY27E/FY28E, led by positive operating leverage and cost-saving initiatives. We estimate the cumulative OCF of INR18.9b over FY27-28 vs. INR5.3b over FY25-26. Estimate cumulative FCF of INR12.9b over FY27-28 vs. cash outflow of INR1.4b over FY25-26. Estimate net cash balance of INR4.5b in FY28 vs. net debt estimate of INR4.4b in FY26E.

* We estimate a normal summer season in FY27. We estimate a UCP revenue growth of ~24% YoY, driven by ~15% volume growth. We estimate the UCP segment margin at 8.2% in FY27. We raise our EBITDA estimates by ~5% for FY27/FY28 (each). Key catalysts to monitor: 1) the onset and intensity of summer in FY27 and RAC volume offtake; 2) liquidation of inventory; 3) order wins in data center and EMP; and 4) margin trajectory.

* At CMP, BLSTR trades fairly at a P/E of 54x/43x on FY27/FY28E. Our SoTP-based TP stands at INR1,950 (valuing UCP/EMPS at 45x each and PES at 25x FY28E EPS). Reiterate Neutral. One-year forward P/E chart Source: MOFSL, Company

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

600-400.jpg)