Neutral Asian Paints Ltd For Target Rs. 2,500 by Motilal Oswal Financial Services Ltd

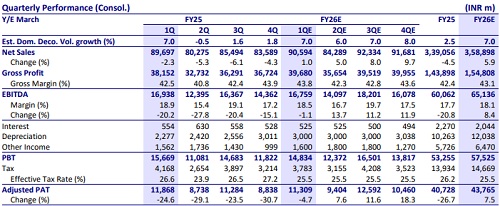

* We model 1% revenue growth in 1Q, as no meaningful improvement has been observed in the demand environment, particularly in urban markets.

* We expect GP margin expansion of 130bp YoY to 43.8% due to deflation in RM prices. EBITDA margin is expected to contract 40bp YoY to 18.5% due to negative operating leverage and high operating costs.

* Volume growth is expected to be 7% in domestic decorative paints. The gap in volume and value growth is due to downtrading.

* We expect this volume-value gap to narrow going forward as demand improves. The price hike taken by company in FY25 also helps in realization growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...