Buy Hexaware Technologies Ltd For Target Rs. 900 by Motilal Oswal Financial Services Ltd

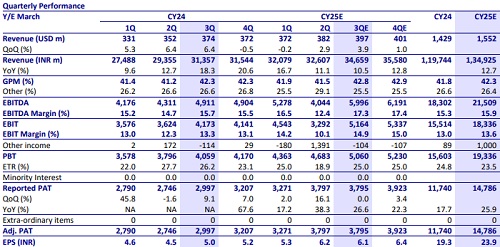

* HEXT is expected to deliver 3.3% QoQ CC growth in 3Q (organic 1.7%).

* FS and Travel & Transportation should lead growth, while Manufacturing and Consumer stay weak; Banking to grow in line with average.

* EBITDA margin (17.3% in 2Q) to remain flat or inch up, led by tapering ERP costs and better offshore mix; guidance should be maintained at 17.1-17.4%.

* Consolidation deal ramp-ups on track, including a large banking engagement; small deals provide steady support. Commentary on demand trends, key accounts’ growth, BFS ramp-ups, and SMC contribution will be key monitorables.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...