Moong Report as On 16 Apr 2026 by Amit Gupta Kedia Advisory

Conclusion

Price Performance: Moong prices declined around 5% over the past month, primarily due to ample carry-forward stocks and rising seasonal arrivals. Increased supply from new rabi crop inflows in key markets has weighed on prices. However, strong export growth and tightening private stocks provide underlying support, limiting the extent of downside despite near-term bearish sentiment.

Domestic Supply Pressure: Supply-side pressure intensified as kharif moong production is estimated at 19.82 lakh tonnes, up 11.72% year-on-year, while rabi pulses production is projected to rise 7%. Fresh arrivals in Gujarat and Maharashtra further increased availability. Additionally, NAFED’s large-scale disposal and buffer stock of 5.40 lakh tonnes continue to cap price upside.

Demand, Trade and Policy Dynamics: Demand conditions remain mixed as moong exports surged 869% to 1.62 lakh tonnes, indicating strong global demand. However, duty-free imports of yellow peas and tur limit substitution demand. Government intervention through MSP at ?8,768/quintal and procurement of 37,020 tonnes provides price support, balancing bearish supply pressures.

Global and Weather Risks: Global and weather factors introduce volatility. China’s mung bean imports rose 109%, intensifying competition, while improved Australian crop outlook adds supply. Conversely, heatwave risks and 60% El Niño probability threaten yields. Early sowing declined 2.9% to 0.95 lakh hectares, indicating potential tightening ahead despite current ample supply conditions.

Technical Outlook: Technical structure remains weak with bearish harmonic pattern on weekly charts and double top formation on daily charts, indicating downside risk. Momentum indicators suggest pressure persists, while volatility remains elevated. However, some stabilization may emerge at lower levels as fundamental tightening gradually offsets technical weakness in the medium term.

Price Outlook:

Performance

Highlights

* Moong prices surged over 7% monthly amid tightening old crop supplies.

* Rainfall in March damaged standing crops across Maharashtra and Rajasthan regions.

* Crop damage reached 195,000 hectares, highest level in last five years.

* Government raised MSP to ?8,768 per quintal for 2025-26 season.

* Moong exports surged 869% during Apr–Jan 2026 period year-on-year.

* China’s mung bean imports jumped 109%, increasing competition for Indian exports.

* India emerging as major global moong export hub with strong shipments.

* Prices dropped 2.5% weekly due to fresh arrivals flooding mandis.

* Moong arrivals rose 62% during Jan–March 2026 compared to last year.

* Summer moong sowing increased 4%, signaling higher supply in coming months.

* Free import policy for tur and urad extended till March 2027.

* NAFED increased buffer stock liquidation, adding pressure on market prices.

* Myanmar pulse inflows stable, reducing supply-side risk premium in market.

* Market entering tightening phase as old crop stocks gradually deplete.

* Heatwave risks and El Niño concerns may impact upcoming crop yields.

* Kharif moong production estimated at 19.82 lakh tonnes, up 11.7%.

* Government maintains buffer stock to control volatility and prevent price spikes.

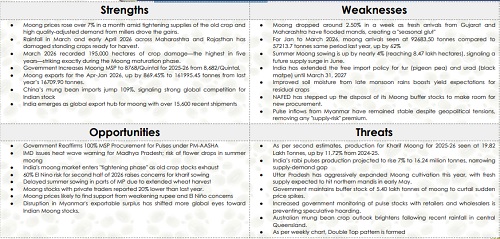

SWOT Analysis