Metals & Mining Sector Update : What`s priced in by Emkay Global Financial Services Ltd

In this edition of ‘What’s priced in’, we highlight that non-ferrous equities show an upside skew to FY27E earnings (particularly VEDL and NACL), on higher spot prices for aluminium, zinc, and silver, while it is largely balanced for HNDL. The ferrous outlook is cautious at current prices, implying a sharp downside risk to earnings if the prices remain lower for longer. However, the market is pricing in a potential price hike cycle with spread improvement of ~Rs3,000/t already baked into estimates for steel equities, with a view that the current downturn is transient. We believe the extension of safeguard duty, coupled with the absorption of excess supply, should catapult into a durable recovery in steel prices, following the transient soft patch due to a domestic steel supply-demand surplus.

Metal equities tend to follow spot earnings momentum closely

At spot commodity prices, we are looking for an upside skew in non-ferrous earnings, particularly for VEDL and NACL with EBITDA upgrade potential of 5.5% and 4.9%, respectively, for FY27E, if spot prices uphold for the entire year. In contrast, our FY27E EBITDA for Hindalco is balanced at spot prices vs our base case, owing to hedges. The key divergence in earnings momentum of these companies stems from healthy prices for industrial metals. If aluminium, zinc, and silver prices stay higher for longer, near-term earnings would be due for an upgrade and work favorably for stock price performance, in our view. Spot aluminium prices are 3% above our FY27 forecast of USD2,700/t, resulting in an upside skew. In ferrous, the market is factoring in price recovery optimism for steel equities, with a view that the current downturn is transient. We believe the extension of safeguard duty, coupled with the absorption of excess supply, should catapult into a durable recovery in steel prices, following the transient soft patch due to a domestic steel supply-demand surplus.

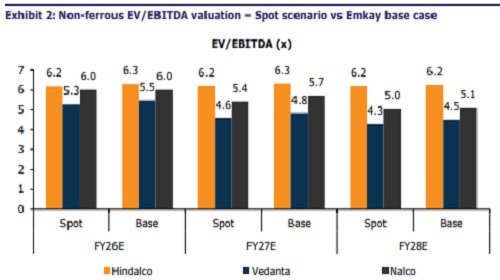

Valuations on spot prices attractive for non-ferrous equities

In our base case, key ferrous names trade at 6-8x FY27E EV/EBITDA multiples. At prevailing spot HRC and long steel prices, the skew to lower EBITDA implies upward pressure on effective multiples, as earnings compress faster than EV adjustments. We see valuations on spot steel prices reflective of trough-cycle multiples, which are not necessarily expensive even if they appear optically. At spot commodity prices, with the upside/downside skew in EBITDA, non-ferrous equities appear better on a relative basis.

What’s priced in

At current stock prices, in the non-ferrous space, the market is effectively discounting commodity prices, which are 7.5% lower for HNDL, 5.2% lower for VEDL, and 3.0% lower for NACL. In the ferrous space, the market is pricing in a potential price hike cycle, with spread improvement of ~Rs3,000/t already baked into estimates.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

NBFC Sector Update : At the crossroads By Emkay Global Financial Services Ltd