Buy Granules India Ltd for the Target Rs. 820 by Motilal Oswal Financial Services Ltd

FDF/API/CDMO drive earnings

Scaling CDMO/complex generics to better business prospects

* Granules India (GRAN) delivered in-line revenue and higher-than-expected EBITDA/PAT (6% beat) for the quarter. Higher formulation (FDF) and API sales led to improvement in overall momentum for the quarter.

* Effectively, GRAN ended FY26 on a strong note after muted performance over FY23-25. This was on the back of increased formulation (FD) sales and product diversification to the complex generics segment.

* Geographically, Europe’s scale-up (+49% YoY Ex-Senn chemicals in 4Q) was due to the launch of complex generics and expanding dossiers.

* The complex generics revenue share has increased considerably from 39% YoY to 46% for 4QFY26. Accordingly, the integrated generics' share reduced from 57% of sales to 50% of sales in 4QFY26.

* GRAN is enhancing prospects in the CDMO segment by integrating R&D at the Zurich and India sites and scaling up manufacturing. Notably, it has achieved EBITDA break-even in the acquired Senn Chemicals business in 4QFY26.

* We raise our earnings estimate by 3%/6% for FY26/FY27, factoring in: 1) the scale-up, driving EBITDA margin expansion of the CDMO peptide business, 2) scale-up of the ADHD portfolio/controlled substances in the US, and 3) the rollout of complex generics and speciality products. We value GRAN at 21x 12M forward earnings to arrive at our TP of INR820. Reiterate BUY.

Product mix/operating leverage drive margins

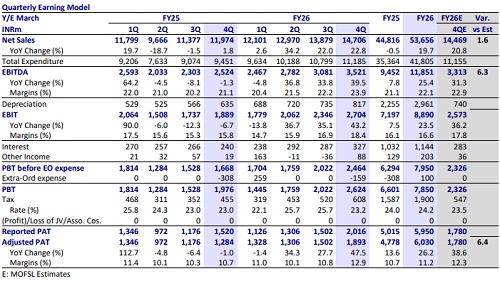

* GRAN’s 4QFY26 sales grew 22.8% YoY to INR14.7b (our est. of INR14.5b), steady momentum in FDF sales/strong growth in API.

* Gross margin (GM) expanded 230bp to 65.7% due to better product mix.

* EBITDA margin expanded 290bp YoY to 24% (our est. of 23%) due to higher gross profit. Higher employee cost (+220bp YoY as % of sales) was offset by lower other expenses (down 275bp as % of sales).

* EBITDA grew by 39.5% YoY to INR3.5b (our est. of INR3.3b) for the quarter.

* Exceptional item in 4QFY26 pertains to gains related to the disposal of investment.

* Adjusted PAT grew by 47.5% YoY to INR1.9b (our estimate: INR1.8b).

* For FY26, Revenue/EBITDA/PAT grew 19.7%/25.4%/26.2% to INR53.6b/INR11.8b/INR6b.

FDF leads momentum/API surges, while CDMO witnesses a sharp QoQ spike

* FDF sales grew 15.5% YoY to INR10.7b (76% of sales).

* Intermediate (PFI) sales grew 8.8% YoY to INR1.3b (10% of sales).

* API sales grew 33.2% YoY to INR2b (14% of sales).

* CDMO sales grew 114% QoQ to INR699m (5% of sales).

Highlights from the management commentary

* The GPI facility in Virginia reached optimal utilization, with ongoing capacity expansion/new distribution center strengthening future growth visibility in the US market.

* GRAN has submitted all action points with respect to remediation measures at the Gagillapur site. The corrective actions were largely completed by Mar'26, and the company awaits USFDA re-inspection. * The CDMO business, through Senn Chemicals, garnered revenue of INR1.6b in FY26 and achieved EBITDA breakeven in 4QFY26.

* Infrastructure ramp-up is underway across geographies for the CDMO business, including the Zurich site upgrade. Notably, Hyderabad R&D center has become fully operational to support Zurich business activities. This would be further supported by the API manufacturing unit at Zurich and intermediates manufacturing in India.

* Nine ANDA approvals are pending from the Gagillapur site, supporting potential US product launches.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412