Buy Castrol India Ltd. for the Target Rs. 220 by Motilal Oswal Financial Services Ltd

Healthy volume momentum; near-term margin pressure

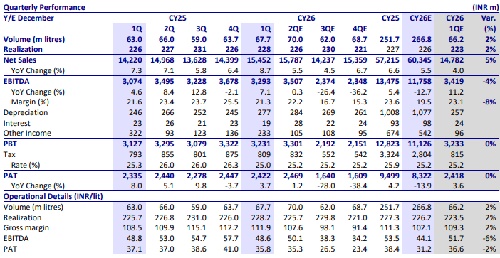

* Castrol’s (CSTRL) 1QCY26 EBITDA/reported PAT came in line with our estimate. While volume grew in high single digits YoY, EBITDA margin contracted 30bp YoY. Reported PAT came in line with our estimate at INR2.4b. Other income came in at 2.4x our estimate at INR233m.

* Key things we liked about the result: 1) Strong volume growth of ~7-8% YoY, indicating healthy underlying demand; 2) Industrial segment delivered robust double-digit growth, while the premium portfolio continued to gain traction; 3) Rural volumes grew at a high double-digit pace, supported by continued expansion in distribution (43,000+ touch points); and 4) Management remains focused on brand building, distribution expansion, and new product launches, which we believe should support sustained volume growth and market share gains.

* Key investor concerns: 1) EBITDA margin at 21.3% came in at the lower end of the guided band, impacted by INR depreciation (~6% YoY) and certain one-off costs; and 2) While gross margins remained resilient in 1Q due to inventory lag, the full impact of elevated crude, base oil, and packaging costs is expected to flow through from 2Q onwards, implying near-term margin pressure.

* CSTRL has always enjoyed a strong brand legacy, and we are confident in its ability to maintain profitability through an improved product mix, stringent cost-control measures, and the launch of advanced products that command better realization. We value the stock at 22x Dec’27 EPS to arrive at our TP of INR220. We reiterate our BUY rating.

In-line performance

* CSTRL’s 1QCY26 revenue stood in line with est. at ~INR15.5b (up 9% YoY).

* EBITDA also came in line with our est. at INR3.3b (up 7% YoY).

* EBITDA margin contracted 30bp YoY (180bps below est.).

* Reported PAT came in line with our estimate at INR2.4b.

* Other income came in at 2.4x our estimate at INR233m. Press release KTAs

* CSTRL broadened its reach and reinforced its presence in the market:

* CSTRL products are distributed through a nationwide network of ~0.15m outlets across general trade, modern trade, and e-commerce channels.

* The service ecosystem is supported by around 800 Castrol Auto Service centers, 34,000 independent bike workshops, and 13,000 multi-brand workshops.

* Rural distribution has expanded to nearly 43,000 outlets, backed by about 700 Rural Service Express centers, driving sustained double-digit growth.

* Over 600 new customers were added, with a strong focus on the mining and electric vehicle segments, including a leading EV two-wheeler manufacturer.

* The company has enhanced its portfolio through targeted innovation and increased localization efforts:

* CSTRL expanded its industrial portfolio with Indian product launches such as Magna 2 (spindle oil), Spheerol EPL 00 (NLGI 00 grease), Hyspin AWS 46 HX (hydraulic oil), and Techniclean 80 XBC (alkaline cleaner).

* It strengthened the Auto Care range with new offerings, including Castrol Ultra Protect Shampoo and Wax, Castrol Dash & Leather Dresser, Castrol Glass Cleaner, an upgraded Castrol Chain Care Kit, and the Castrol Bike Engine Shampoo (flush).

* It signed an MoU with HPCL to explore the development of a re-refined base oil ecosystem in India.

* The company improved consumer relevance through impactful engagement initiatives:

* CSTRL mobilized large rider and enthusiast communities, including 3,000+ participants at Spirit of Unity 3.0, over 500 women riders through the #MorePowerToYou campaign, 18,000+ attendees at the V12 Kakkoor Kalavayal Moto Festival, and 1,200+ riders via Road Trip United.

* The company strengthened brand positioning with the launch of the corporate film Har Boond Mein Desh Ki Raftaar, highlighting its contribution to the nation’s progress and building a deeper emotional connection with consumers.

* Its digital engagement ecosystem was expanded with FastScan (the verified mechanic network) growing to 164,000 members, marking a 30% YoY increase.

Valuation and view

* We build in EBITDA margins of 19.5%/22% for CY26/CY27, below the company’s guided range of 21-24%, as we factor in the impact of a sharp rise in crude oil prices and ongoing supply chain disruptions, which are likely to exert near-tomid-term pressure on profitability. Further, we build in volumes to clock a 6% CAGR over CY25-27, primarily driven by strong growth in the industrial and rural segment. The stock currently trades at 18.5x CY27 EPS with 5% dividend yield and ~50% RoE/RoCE in CY27.

* We value the stock at 22x Dec’27 EPS to arrive at our TP of INR220. We reiterate our BUY rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)