Mauritius at risk: Macroeconomic implications of oil price volatility by CareEdge Ratings

Mauritius: Economic spillovers from the Middle East conflict

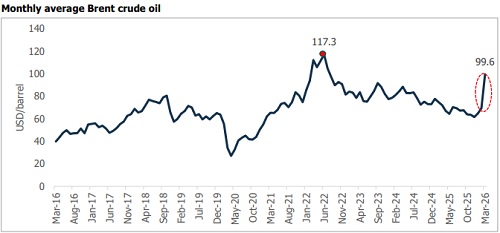

The ongoing Middle East conflict continues to fuel volatility in global energy markets. Despite recent diplomatic efforts and attempts at de?escalation, lasting stability remains elusive. Renewed military activity and disruptions to key maritime corridors have kept energy markets on edge, maintaining a risk premium on oil prices.

All eyes are on the Strait of Hormuz, a critical conduit for global oil and gas trade. Periodic restrictions on maritime passage, higher war?risk insurance premia, and elevated freight costs have reinforced concerns over the reliability of energy supply routes. Resultantly, global crude oil prices remain elevated and volatile, with risks leaning towards instability rather than normalisation.

Energy import?dependent economies such as Mauritius are intensely affected. Higher and more volatile oil prices raise import costs directly and indirectly through freight, insurance, and commodity price channels, adversely affecting domestic inflation, external balances, and growth prospects. Even under a favourable scenario where geopolitical tensions ease intermittently, we are of the view that conflictinduced cost pressures are unlikely to normalise in the near term, implying sustained downside risks for Mauritius.

Oil price scenarios and effect on the Mauritian economy

For a small, open, and import-dependent economy such as Mauritius, changes in global oil prices affect the macroeconomic outlook through a set of transmission channels. Higher oil prices raise the fuel import bill directly, while driving up freight and insurance costs across imports. These cost pressures also spill over into other domains with increasing fertiliser, transport, and distribution costs, which ultimately raises domestic inflation.

Concurrently, higher energy and logistics costs weigh on household purchasing power and business profitability, ultimately slowing down growth. On the external side, rising import values widen the trade and current account deficits, increasing reliance on external financing and pressure on foreign exchange buffers.

Against this backdrop, we have analysed the macroeconomic outlook under pre-crisis and three oil price scenarios. While each scenario shares the same economic transmission channels described above, outcomes differ in terms of the scale and duration of the shock.

The pre-crisis scenario is included as a reference case, consistent with the IMF’s initial 2026 outlook (October 2025), when crude oil prices were expected to average USD 66 per barrel and global energy markets were assumed to remain stable. This scenario provides a counterfactual benchmark for assessing how recent developments have altered the macroeconomic outlook.

Scenario?1 is assessed as the baseline and most likely outcome, reflecting current market conditions and prevailing geopolitical uncertainty. Under this scenario, crude oil prices are assumed to average USD 82 per barrel in 2026, remaining elevated relative to pre-crisis expectations and resulting in persistent but manageable pressures on inflation, growth, and the external position.

Scenarios 2 and 3 explore progressively more adverse environments under sustained high oil prices. Scenario?2 assumes crude oil prices averaging USD 95 per barrel, while Scenario?3 represents a more extreme stress case with prices averaging USD 105 per barrel. While the transmission channels are unchanged, higher price and greater persistence of the shock result in increasingly binding cost pressures, wider external imbalances, and more pronounced macroeconomic adjustment.

Macroeconomic impact across oil price scenarios Inflation

After averaging 3.7% in 2025, the IMF’s October 2025 WEO forecast inflation in Mauritius to remain stable at 3.6% in 2026, contingent on broadly stable external conditions. Consistent with this outlook, higher?frequency data showed a period of near?term disinflation in early 2026, with headline inflation easing to 2.7% YoY in March, from 3.5% in February and 3.9% in January. This stems from a temporary slip in food and energy prices alongside lagged effects of administered price measures.

However, benign near?term disinflation is unlikely to last amid escalating geopolitical tensions and sustained increases in international oil prices. Because petroleum products, including petrol, diesel, LPG, jet fuel, and fuel oil for electricity generation accounted for 22.9% of Mauritius’s import bill in 2025, the economy is highly sensitive to oil market volatility. Higher crude oil prices, therefore, transmit rapidly into inflation through higher retail fuel prices, rising transport and freight costs, and increased production expenses. This transmission is reinforced by the high weight of fuel and lubricants for personal transport equipment (7%), and electricity and cooking gas (3.9%) in the CPI basket. The initial shocks are subsequently amplified through second?round channels, particularly via food distribution, services, and informal economic activity.

Under the pre?crisis reference case, where oil prices were assumed to average USD 66 per barrel, inflation was projected at 3.6%, broadly consistent with medium?term price stability.

Against this benchmark, Scenario?1 (baseline), which assumes USD 82 per barrel, sees inflation rise to 4.9% in 2026. This projection is consistent with price pressures already materialising domestically, including cumulative increase of 20.9% per litre in diesel prices in March and April 2026 (reflecting two consecutive adjustments), a 9.9% increase in petrol prices per litre in April 2026, and a 31.6% rise in cooking gas prices (LPG 12kg) in April 2026. In addition, administered food prices have been adjusted sharply, with the price of a 100g loaf of bread increasing by 50% in April 2026, alongside an expected 15% increase in electricity tariffs from May 2026. Collectively, these developments raise the costs for households as well as firms, reinforcing the upward inflationary trajectory under the baseline scenario.

Under Scenario?2 (USD 95 per barrel), inflation is projected to rise to 6.0% in 2026. Under Scenario?3 (USD 105 per barrel), inflation is expected to increase to 6.8%.

Overall, while headline inflation (YoY) moderated temporarily in early 2026 (January-march), the balance of risks has shifted decisively to the upside. Sustained oil price pressures are expected to reverse recent disinflation and lift inflation above pre?crisis expectations as prices consistently trend up.

Above views are of the author and not of the website kindly read disclaimer