Logistics Sector Update : Feb-26 – Freight and cargo monthly by Emkay Global Financial Services Ltd

In this monthly edition, we highlight high-frequency data points to assess freight and cargo movements across multiple modes of transportation. In Feb26, Indian ports saw moderation in growth momentum, with a 3% YoY increase (5% YTD), as major port volumes grew ~4% YoY, while non-major port volumes grew ~2% YoY. Within this landscape, Adani Ports (BUY) successfully gained market share, reporting superior volume growth of 16% YoY (14% YoY for containers, vs 8% for the overall industry). On the domestic logistics front, GST e-way bill volumes saw a marginal 1% MoM uptick (3mma)—tempered primarily by the shorter calendar month—while truck freight rates remained firm, supported by stable diesel pricing. However, the global landscape has shifted rapidly with the ongoing Middle East (ME) conflict. With the Gulf region being a major maritime hub, the current disruption of trade activities in the region led to a spike in container shipping rates in Mar-26 (up 14% from Feb26 lows). We believe this may impact trade volumes as cost of transportation increases.

APSEZ, JSW Infra volumes at risk given exposure to ME

APSEZ and JSW Infra both face direct and indirect risks to volumes, owing to their international assets and disruption in trade linked to the ME. For APSEZ, direct exposure is centered on the Haifa Port in Israel, which contributes 2%/5%/2% to volume/revenue/EBITDA (9MFY26), respectively. Continued hostilities here pose a direct threat to volume stability and margin health through increased insurance premiums and operational security costs. Further, as per the management, 15% of Mundra’s container volumes are linked to the ME, and 50% of the crude and gas portfolio is linked to the Strait of Hormuz. The ME crisis also has a direct impact on APSEZ’s marine segment (Astro business) and the international freight forwarding business (9MFY26 revenue contribution 7%/2%, respectively). We believe any escalation that restricts access to this critical maritime chokepoint is likely to result in volume contraction and margin compression, given the hike in freight rates and supply chain bottlenecks. JSW Infra (ADD) has experienced a tangible escalation in operational risks as the regional conflict extends toward the Gulf of Oman. This is evidenced by the recent drone incident at its Fujairah Liquid Terminal, damaging one of its 15 storage tanks. While physical damage was contained, the event underscores the vulnerability of the company’s ME footprint, which contributes 6%/7% to volume/revenue (FY25), respectively. Given that the Fujairah liquid business is a high-margin segment, any disruption could lead to a disproportionate compression of profitability, in our view.

Container shipping rates rose sharply, with the Gulf closed due to the conflict

As per the Drewry WCI Index, container shipping rates have spiked 13% MoM (as of 19- Mar-26), driven by severe structural disruptions following the closure of the Strait of Hormuz. This geopolitical escalation has triggered a critical supply-demand imbalance, as a significant portion of the global fleet remains stranded or diverted – unable to access the Gulf region. While higher logistics costs are already dampening demand for nonessential trade items, the primary headwind remains the restricted vessel supply. Industry consensus suggests that these prolonged bottlenecks will lead to sustained volatility in freight rates, weighed down by compromised volume throughput and extensive global supply chain inefficiencies.

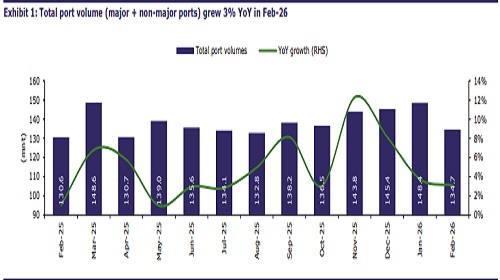

Port volume momentum moderates

India’s port sector maintained a positive trajectory in Feb-26, with major port cargo volumes growing 4% YoY. This reflects sustained growth in trade activities and improving infrastructure on the domestic front. Volume growth was led by Coal (up 5% YoY) and Containers (up 10% YoY). Ports such as Vizag (+24% YoY), Mumbai (+15%), JNPT (+11%), and Kandla (+7%) too witnessed robust volume growth in Feb-26, though Kolkata/Cochin/Tuticorin ports saw 11%/11%/4% YoY decline in volumes, respectively. Non-major ports continued to see moderate growth (+2.3% YoY) over the same period. Container volumes sustained positive momentum, growing 8% YoY, led by 11% growth at JNPT (JNPT market share thereby increased, from 24.2% in Feb-25 to 24.8% in Feb-26).

GST e-way bill volume trajectory maintained

GST e-way bill volumes grew in Feb-26 (up 19% YoY), albeit declining 3% MoM, largely on account of a smaller month. Intra-state volumes were up 22% YoY, while inter-state volumes grew 14%. Truck freight rates were steady across major trunk routes, as diesel prices were unchanged.

Momentum in manufacturing and key commodity production remains strong; ongoing war remains a key monitorable

Steel production grew ~7% YoY, while coal production increased ~2% YoY. The cement sector too demonstrated positive momentum, with ~9% YoY growth in Feb-26. We expect the sector to witness robust momentum, given the higher capex allocation for infrastructure projects in the Union Budget 2026-27. Manufacturing PMI expanded to 56.9 in Feb-26 (Jan-26: 55.4). This uptick in commodity production volumes points to favorable demand tailwinds for port operators and logistics companies, as higher manufacturing activity typically translates into increased freight and cargo handling opportunities. However, with the ongoing crises owing to the conflict in the ME, the limited supply of energy (alternatively, energy being procured at a higher price) is likely to lead to higher raw material costs, which might hamper demand and margins for manufacturing companies.

Rail freight – WDFC nearing completion

While rail freight tonnage recorded a modest 2% YoY increase in Jan-26, the overall sectoral performance remains tempered due to infrastructure bottlenecks that have hindered both coal and container volumes. Despite the Eastern Dedicated Freight Corridor (EDFC) being operational since >2 years, coal cargo (~49% of the total Jan-26 freight tonnage) has yet to see a substantial uptick, with the RSR route being the key mode of transport for coal. Container freight grew a sluggish 4% YoY due to the unfinished final stretch of the Western Dedicated Freight Corridor (WDFC). However, a significant inflection point is on the horizon. With the WDFC slated for full completion by Mar-26 (~93% complete as of Dec-25), we anticipate brisk acceleration in rail volumes. We believe this expanded capacity is likely to unlock a surge in freight traffic, offering logistics players a clear runway for robust earnings visibility and revitalized growth.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354.

More News

Automobiles Sector Update : Auto Sales Soar as Rain Pours by PL Capital