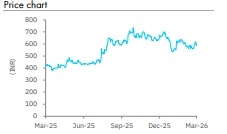

Buy BlackBuck Ltd For Target Rs.814 By Elara Capital

Fortified core powers SuperLoads acceleration

BlackBuck (BLACKBUC IN) is entering a multifold monetization phase . Its stabilized core business – payments and telematics (92% of revenue as o n FY25) – is set to compound through market share gains, industry tailwinds, operating leverage , and robust profitability. Mean while , growth initiatives like SuperLoads are monetiz ing digital freight transactions via platform , positioning BLACKBUC as an end -to-end solution for 3.5mn truck operators in a USD 135- 140 bn unorganized freight opportunity . Core profit s would fuel SuperLoads ’ expansion, with an established playbook, targeting ~10x revenue by FY28 E via replication . T he company is reshaping India’s trucking ecosystem. We i nitiate with a Buy rating , with DCF -based TP of INR 81 4, assuming INR 665 for the core business and INR 149 for SuperLoads .

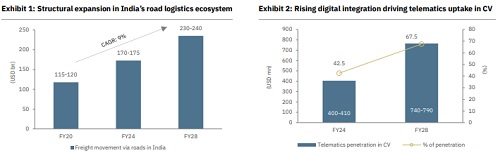

Core segment leadership during 10 years with ~INR 15bn investment: Since FY 15, BLACKBUC has built a dominant platform for truck operators through expand ed offerings , capturing 48% market share in CV toll ing with ~1mn annual transacting users (~68% monthly active with ~44 minutes daily app engagement), and a distribution network of 10k+ touchpoints covering ~80% of districts. This scale drives cross -selling and slash es customer acquisition cost. We expect core payments (Gross T ransaction V alue ) CAGR of ~20% during FY25 -28E (~21% revenue CAGR) , fueled by rising take rates, transaction growth , market share gains from banks, and structural tailwinds , such as NH expansion, toll hikes of ~4 – 5% are typically linked to WPI , and CV growth – sustaining ~92 -93% contribution margin and ~33% adj EBITDA margin as of 3QFY26 .

SuperLoads, the growth engine: SuperLoads (digital freight -matching marketplace) targets India’s ~USD 1 35-140bn unorganized road freight market, dominated by ~25 0K informal brokers handl ing 7 00-800K long -distance truckloads daily – of which a mere ~7 – 8% is digitized . Operati ons scaling to nine hubs, it delivers ~INR 200mn GTV and ~INR 10mn revenue at ~5% commission as on Q3FY 26. We expect expansion to ~30 hubs by FY28 E , unlock ing ~INR 10.7bn GTV (~INR 538mn revenue), via higher freight density, longer haul s, and better backhaul utilization – reaching EBITDA breakeven by FY30 E as transaction density per agent improves .

Platform transition unlocks operating leverage: The FY17 shift from enterprise freight to transaction -led digital platform slashed working capital days and stabilized core earnings. As scale builds up , operating leverage is set to drive positive PAT from FY26E and strong free cashflow generation with a FCF yield improving to ~1.1 -1.4% during FY26 – 28E under an asset -light , net cash model . In the long term, growth business es to amplify value creation .

Initiate with Buy and a TP of INR 814: Near -term earnings hinge on the core segment while SuperLoads drives long -term growth , potentially contributing ~33% of revenue by FY40E , fueling ~23% net revenue CAGR during FY25 -40 E . Margin may moderate to ~28 -29% by FY28 E amid reinvestment s, but 90%+ contribution margin in the core businesses should ensure robust cash flow. We initiate with a Buy rating and DCF -based TP of INR 81 4 implied 53x FY28E EV/EBITDA. We assume a WACC of 12%, a terminal growth rate of 5%, a revenue CAGR of 31 % and an EBITDA CAGR of 40% during FY25 -28E .

Investment Rationale

Dominant commercial vehic ular tolling franchise with rising market share, where deepening multi -product engagement across payments and telematics is driving operating leverage and structurally expanding recurring earnings SuperLoads offers scalable freight optionality, monetizing India’s large unorganized road freight logistics market of USD 1 35-140mn as on CY 24 Profitable core platform economics provide earnings visibility, with SuperLoads expansion adding asymmetrical growth potential.

Valuation triggers

* BLACKBUC to post consolidated net profit in FY26 for the first time

* Disciplined scaling up of SuperLoads w ould unlock incremental valuation upside

* Continued margin expansion and robust cashflow from the core platform would drive growth

Our assumptions

* Consolidated net revenue CAGR of 31% during FY25 -28E , led by 27% CAGR in the core business and 64% in the growth business

* We assume EBITDA CAGR of 40% during FY25 -28E.

Key risks (downside)

* Any adverse change in toll fees economics could compress take rates .

* Scaling up SuperLoads without slipping into capital intensity or operational complexity remains critical .

* Banks, fintech, or digital freight platforms could put pressure on market share and moneti zation.

Please refer disclaimer at Report

SEBI Registration number is INH000000933