Buy Kolte Patil Developers Ltd for the Target Rs.450 by Motilal Oswal Financial Services Ltd

Growth expected to revive in the coming quarters Presales growth expected in FY27

* 4QFY26 presales grew by 13% YoY to ~INR7.1b (vs. our estimate of CINR6.2b), driven by a strong response to new launches, along with sustenance sales. Consequently, quarterly pre-sales crossed the INR7b mark again after five quarters. Life Republic continued to anchor demand, contributing 43% to pre-sales during the quarter. Pune projects contributed 75% to pre-sales, while the Mumbai portfolio saw healthy traction from projects in Versova (INR500m), Goregaon (INR500m), and Santacruz (INR380m) in 4QFY26. Overall, in FY26, presales declined 7% YoY to ~INR26.1b.

* We note that KPDL’s pre-sales have remained in the range of INR26-29b in the last three years. However, given the comfortable launch pipeline, healthy demand and realignment of focus on operations with the Blackstone deal largely completed, we expect presales CAGR of 17% to INR35.5b in FY26-28E.

Comfortable launch pipeline

On the BD front, KPDL acquired projects with an aggregate GDV of INR22.5b (3msf salable area) in FY26. It has 4.7msf of ongoing and unsold projects and 7.6msf is under approval across various projects, of which 89% is in Pune. It also has availability of an additional land bank admeasuring ~24msf in Pune and Mumbai, building a strong launch pipeline. The aggregate development potential of 36.7msf offers an estimated GDV of ~INR293b, which provides comfortable visibility on presales growth over the medium term

Healthy collections; sturdy balance sheet

Collections grew 18% YoY to ~INR8.3b in 4Q and 11% YoY to INR27b in FY26, which is encouraging despite a decline in presales. In FY26, KPDL generated OCF of INR7.9b, with net cash of INR5b (including zero coupon bonds, net debt stands at INR1.6b). On the back of presales growth and project execution in the next two years, we expect collection CAGR of 18% to INR37.7b in FY26-28E. We expect net debt at INR2.0b/INR2.3b in FY27/28E.

P&L highlights

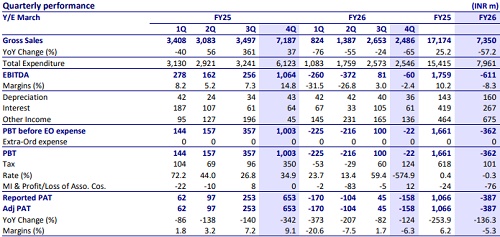

* In 4Q, revenue stood at INR2.5b, declining 65% YoY. EBITDA loss stood at INR60m vs. positive EBITDA of INR1.1b YoY. PAT loss stood at INR158m vs. a profit of INR653m YoY.

* In FY26, revenue stood at INR7.4b, declining 57% YoY. EBITDA loss stood at INR611m vs. positive EBITDA of INR1.8b YoY. PAT loss stood at INR387m vs. a profit of INR1.1b YoY.

Valuation and view

* Presales have been sluggish in the last three years and are expected to revive in FY27 since management-level transitions related to the Blackstone deal are largely completed. KPDL also has a healthy launch pipeline, which provides growth visibility over the medium term. Collections have remained strong despite sluggish presales, and hence, we expect the balance sheet to remain sturdy as progress in execution remains healthy.

* We reiterate BUY with a TP of INR450, indicating a potential upside of 19%.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412