Buy Midwest Ltd for the Target Rs.1500 by Motilal Oswal Financial Services Ltd

In-line earnings; Quartz ramp-up deferred for near term

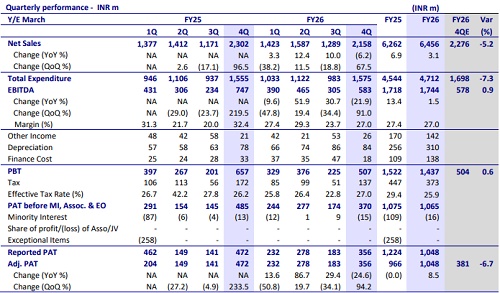

* Midwest reported revenue of INR2.2b in 4QFY26, down 6% YoY and in line with our estimate. Revenue rebounded by 68% QoQ, led by strong volume and price recovery.

* Black galaxy granite production stood at 29.1k cbm (+90% QoQ), while absolute black granite stood at 9.1k cbm (-4% QoQ). The company sold 26k cbm of black galaxy granite (+75% QoQ) and 9.2k cbm of absolute black granite (+2% QoQ). The blended granite ASP was INR60,792/cbm (+13% QoQ) in 4QFY26.

* EBITDA came in line at INR583m, down 22% YoY but up 91% QoQ. This translated into EBITDA margin of 27% in 4QFY26 vs. 23.7% in 3QFY26 and 32.4% in 4QFY25.

* APAT came in at INR356m vs. our estimate of INR381b, down 25% YoY but up 94% QoQ in 4QFY26.

* In FY26, revenue stood at INR6.5b (+3% YoY) and EBITDA was INR1.7b (+2% YoY) with a margin of 27% vs. 27.4 in FY25. APAT grew by 9% YoY to INR1b. ? Black galaxy granite production came in at 76k cbm (+14% YoY) and sales stood flat YoY at 73k cbm in FY26. The absolute black granite production stood at 40k cbm (+4% YoY), while sales were down 6% YoY at 40k cbm. The average sales price in FY26 stood flat YoY at INR57,400/cbm.

Key highlights from the management commentary

* Management expects granite to contribute about 10-12% organic CAGR, targeting INR4b from Quartz (two phases + HPQ), INR3.5-4.0b from HMS in Sri Lanka (Phase 1), and INR2b from the commercialized KMML project.

* For FY27, the Quartz Phase 1 plant aims to reach at least 60% of its 250KT rated capacity in a phased manner. The Phase 2 is expected to be commissioned in 4QFY27, with contribution to start from 1QFY28.

* Quartz Phase 1 products are priced at INR7,000/t for solar grade and INR9,000-14,500/t for engineered stone.

* Granite margins are expected to remain stable, with marginal improvement from cost optimization. Quartz margins are anticipated to improve once capacity utilization reached 60-70% with both phases fully operational.

* Capex for the Quartz Phase 2 plant will be INR1.25-1.30b, with construction having started in Apr’26 and commissioning targeted for 4QFY26.

* Capital outlay of INR200m is allocated for the KMML rare earth pilot plant, which is expected to start in early Jul’26.

Valuation and view

* Midwest delivered decent earnings as anticipated in 4Q, mainly supported by strong volumes and ASP recovery. We cut our FY27 revenue/EBITDA/ APAT estimates by 18%/21%/23%, factoring in the delay in phase-1 rampup of Quartz business.

* We expect Midwest to clock a 57% revenue CAGR over FY26-28, led by the new business venture (Quartz and Heavy Sand Minerals), translating into a CAGR of 77% in EBITDA and 87% in PAT. We expect the quartz segment to contribute ~33% of the total operational revenue in FY28, thus diversifying from granite.

* The company’s debt-to-equity ratio is expected to remain favorable. The recent debt repayments have helped the company achieve a net cash status.

* At CMP, Midwest trades at 8x FY28E EV/EBITDA. We reiterate our BUY rating on the stock with a revised TP of INR1,500, valuing the stock at 10x FY28E EV/EBITDA.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412