IT Sector Update : Risks are Understandable;Though Exaggerated; Time to Buy Midcaps by by Choice Institutional Equities

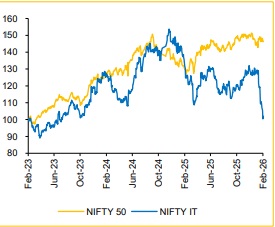

Valuation Reset Creates Selective Midcap Opportunity

The recent correction across IT services, ER&D and SaaS appears primarily valuation-led, reflecting lower terminal growth assumptions amid AI disruption concerns rather than a sharp deterioration in near-term fundamentals. While markets are pricing a deflationary end-state, enterprise AI adoption is likely to be gradual and execution-intensive, sustaining multi-year spend across cloud modernisation, data infrastructure rebuilds and AI-enablement programmes even as effort-based revenue pools face medium-term headwinds. Critically, meaningful AI deployment requires substantial upfront investment in cloud migration, data governance and integration, a readiness cycle that we believe expands the addressable IT TAM before productivity-led deflation can fully materialise, and one that IT services vendors are structurally positioned to monetise. Against this backdrop, we see selective opportunity emerging in quality midcap & small caps where structural growth differentials remain intact, but valuation premiums have largely normalised; riskreward appears increasingly asymmetric on a 12–18-month view as the sector pivots toward outcome-led, platform-centric delivery models. Overall, we view the sector as entering a structural transition phase where growth normalizes but demand remains supported by large-scale modernization and AI-enablement programs, with long-term winners defined by their ability to pivot toward outcome-led, platform-centric delivery models. Our long-term investment ideas are COFORGE, PSYS, HAPPSTMN and KPITTECH.

AI Transition, Not Disruption: Valuation Reset Creates Selective Opportunity

The recent correction across IT, ER&D services and SaaS company reflects a valuation-led reset driven by lower terminal growth expectations amid rising AI-led disruption concerns, rather than a material deterioration in near-term fundamentals. While markets are increasingly pricing a deflationary end-state, we believe the transition toward enterprise AI adoption will be gradual and execution-intensive, creating meaningful opportunities across legacy modernization, migration of legacy SaaS applications, enterprise AI foundation-layer buildouts and emerging physical AI use cases. AI-driven productivity gains are likely to compress effortbased revenue pools over time; however, improving deal momentum over the last 12 months, easing client-specific headwinds and rising enterprise urgency to deliver AI outcomes suggest business velocity is improving. Overall, we view the sector as entering a structural transition phase where growth normalizes but demand remains supported by large-scale modernization and AI-enablement programs, with long-term winners defined by their ability to pivot toward outcome-led, platform-centric delivery models

AI Productivity to Gradually Reshape IT Services Economics

AI represents a structural shift rather than an immediate disruption for IT services, as enterprise environments remain complex across legacy backend systems, data architecture and customer-facing layers, sustaining demand for systems integrators in modernisation and transformation programs. That said, AI-led productivity gains are likely to introduce a gradual structural deflationary impact, with industry estimates suggesting a 2–3% revenue headwind over the next 2–3 years, peaking around FY27E as automation reduces effort intensity across contracts. This dynamic is accelerating the transition away from traditional time-and-material models toward outcome and value-based engagements, weakening the historic linkage between headcount and revenue while favouring vendors capable of delivering measurable business outcomes through AI-enabled execution. This shift arguably favours mid-sized, digital-native players with leaner operating models and faster decision cycles, particularly in engineering-heavy transformation mandates

Margins Likely Resilient Despite AI-Led Deflation Risks

Despite AI-led revenue deflation risks, margin are likely to remain resilient in the near to medium term as vendors leverage automation, pyramid optimization and consolidation benefits, implying stable earnings even as growth moderates. The impact of AI will be uneven across service lines, with software engineering, applications and customer support facing higher disruption, while infrastructure management, brownfield programs and vertical-specific BPO remain relatively insulated due to operational complexity and slower agentic AI adoption. Importantly, enterprise AI deployment requires significant upfront investments in cloud migration, data modernisation and governance, positioning IT services firms to benefit from a multi-year readiness cycle that could expand the overall IT TAM before productivity-led deflation fully materialises.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131