IT Sector Update : 4Q likely uneventful but AI deflation and war risks keep outlook uncertain by Motilal Oswal Financial Services Ltd

* After a whirlwind couple of months (NSEIT down 23% YTD), driven by narrative shocks, we expect 4QFY26E numbers to be somewhat uneventful: we see no major disruptions from the ongoing war on numbers yet (although deal wins may be impacted in the short term), and we do not see major evidence of deflationary shocks from AI implementation yet.

* However, we concede that both these data sets are backward-looking. If the war persists, demand is likely to be affected, whereas AI deflation is more a question of what AI will be capable of in the next two to five years, rather than the last quarter.

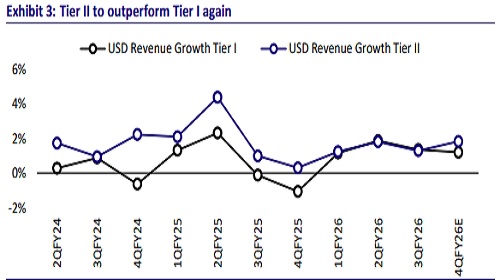

* 4Q results are likely to mirror this set-up, with QoQ cc growth expected in the range of -1.0% to 1.5% for large-caps, and mid-caps expected to outperform once again with a growth range of -0.5% to 3.5%. For 4Q, we expect aggregate revenue for our coverage universe to grow by 11.3% YoY, while EBIT and PAT are likely to grow by 12.9% and 10.8% YoY (all in INR terms), respectively.

* On guidance, exit rates for most large-caps now appear relatively favorable. We expect organic YoY CC growth exits of 4.3%/4.9% for INFO/HCLT in 4QFY26. However, we expect companies to exercise caution in light of the current geopolitical environment. We expect INFO to guide FY27 revenue growth of 1.5– 4.5% YoY CC. The CQGR ask at the lower end is 0.5%, allowing for some deterioration in macros and headwinds from the Daimler ramp-down. There is potential for an upgrade if they backfill Daimler through the year.

* For HCLT, 3–6% YoY cc growth is expected for services. The top-end assumes mild improvement in CQGR over FY26E, while the bottom end assumes uncertainty from war. We expect products to be flat to slightly declining in FY27.

* We expect margins to be range-bound for TCS, INFO, MPHL, and PSYS. We expect a margin contraction for Wipro (Harman DTS dilution, wage hikes, slower growth) and HCLT (wage hikes, restructuring headwinds and P&P decline). Among mid-caps, Hexaware and LTTS may see ~40bp/~60bp pressure due to ramp-ups, seasonality, and wage hikes. Weak INR vs USD should support margins.

* We expect INFO to maintain 20–22% margin guidance. However, we believe that slower-than-expected product growth, along with pressure from productivity, puts HCLT's expectations of returning to the 18-19% margin band at risk.

* Vertical performance in 4Q: BFSI remains relatively resilient. Manufacturing is mixed - Auto OEMs are adjusting to tariff risks, but spends remain elusive. Hi-Tech is broadly flat. Travel & Transportation is likely to be impacted by war-related concerns, with some engagements facing delays.

* Since we upgraded the sector multiples in Nov '25, numbers and narrative have diverged to extremes; the sector has seen earnings/guidance upgrades in 3Q, but the narrative shock from Anthropic launches (see our report dated 13th Feb, 2026: Indian IT services: Assessing the narrative shock) has led to a brutal compression of multiples. While the fears around terminal value are difficult to validate or falsify, the burden of proof now sits with IT services. Re-rating, thus, depends on proof of surviving and thriving. We, thus, cut our target multiples by 30-40%.

Growth expectations across our coverage

* We expect revenue growth of 1.5% QoQ CC for TCS and 1.0% for WPRO, driven by a two-month inorganic contribution from the Harman acquisition. INFO/HCLT are likely to report 0.7%/0.9% revenue decline in 4QFY26, due to 2H being weaker than 1H as front-ended growth/seasonality in software. TECHM may post 0.5% QoQ growth, while LTIM could report 1.5% CC growth, aided by continued large-deal ramp-up.

* Among mid-tier firms, PSYS may lead with ~3.5% CC QoQ growth. COFORGE/MPHL could deliver 1.5%/2.5% growth. HEXT may decline 0.5% CC due to seasonality and delayed deal closures.

* Among ER&D names, we expect steady numbers. KPIT may report 1.0% QoQ CC growth, while TTL could report 9.5% QoQ CC (inorganic ~4.5% + recovery in core). TELX/LTTS may see 2.0%/1.2% growth.

* We expect Cyient DET to report 2.1% CC growth, as some stabilization is expected.

* Cross-currency impact for the quarter: On average, we expect ~10-40bp crosscurrency tailwinds for our coverage on a sequential basis.

Margins a mixed bag

* We expect TCS/INFO EBIT margins to be range bound in 4Q. We expect HCLT margins to contract ~140bp QoQ, driven by wage hikes, restructuring headwinds and high-margin P&P decline.

* We expect TECHM to see ~50bp margin expansion, driven by fixed-price project optimizations leading to gross margin gains. We expect LTIM margins to contract ~90bp QoQ due to wage hikes, fewer working days, and client productivity programs.

* Among mid-caps, COFORGE margins could see an expansion of ~160bp QoQ to ~15.0%, as wage hike headwinds are behind. MPHL/PSYS are likely to hold margins range-bound. Zensar should see ~220bp decline as earlier one-offs benefits and efficiencies fade, along with lower revenue growth.

* For ER&D companies, margins are estimated to remain flat or improve, except TELX, which should see a decline due to wage hikes in 4Q.

INFO and COFORGE remain our top picks

* Among large caps, we prefer HCLT and Tech Mahindra, while COFORGE remains our top mid-cap pick.

* We like HCLT as the company remains the fastest-growing large-cap IT services firm, and we like its all-weather portfolio, which continues to outperform in an uncertain demand environment. At current valuations, upside risks meaningfully outweigh downside risks. For TECHM, we see signs of transformation under the new leadership and improving execution in BFSI. We believe TECHM’s transformation remains relatively decoupled from discretionary spending.

* In mid-caps, COFORGE remains our top pick. We believe COFORGE’s strong executable order book and resilient client spending across verticals bode well for its organic business. Encora’s acquisition expands COFORGE’s presence in the Hi-Tech and Healthcare verticals. We continue to view COFORGE as a structurally strong mid-tier player well-placed to benefit from vendor consolidation/cost-takeout deals and digital transformation.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Banks: The Achilles` heel for banks: Sluggish deposit momentum by Kotak Institutional Equities