Geopolitical Risks and 15% Earnings CAGR Shape Nifty Outlook at 27,080: PL Capital

PL Capital, one of the most trusted financial services organisations in India, in its recently published India Strategy Report, says that the current growth path of India is entering in challenging phase due to increasing geopolitical tensions, growing cost of crude oil, and disruptions in the global supply chain. Though the drivers of economic growth continue to remain the same, the factors that affect them externally have increased and hence, earning projections are being lowered.

As per PL Capital’s study, The Nifty has fallen by 6.6% over the last three months due to continued foreign institutional investor (FII) redemptions against the backdrop of geopolitical instability, especially the West Asia crisis. Though there has been a significant rally after touching the lowest levels recently, market conditions remain choppy on the back of global risks and increasing commodity prices. The earnings visibility outlook has improved marginally, with an expected 4% growth in Nifty EPS for fiscal year 26. The medium-term forecast suggests a compounded annual growth rate (CAGR) of 15% over fiscal years 26–28.

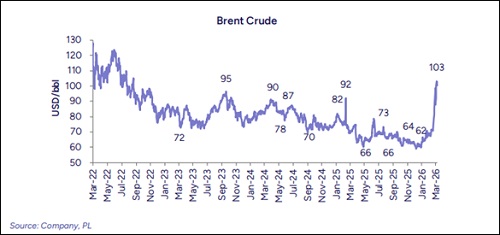

The macro environment in India is seeing new challenges arising due to high oil prices, where the country imports around 85% of its total oil needs. The rise in the price of crude oil will lead to higher costs in the import of oil by over $70 billion each year, which may lead to inflation rising above 5%. Furthermore, disruptions in the supply chain and the possibility of El Niño effect on the monsoon season might lead to inflation becoming higher. Growth in GDP is currently at around 6.5% and can further dip to 6%.

Oil prices have seen a sharp spike and are unlikely to revert to pre-war levels. India, which imports 4.3 million barrels of crude per day (valued at USD 180 billion), could see its import bill rise by over USD 70 billion annually. While supply chain realignments and diversification of import sources may provide some relief, key shipping routes such as the Strait of Hormuz remain critical risk factors.

The impact of higher crude prices is expected to be relatively lower than past shocks due to reduced oil and gas imports as a percentage of GDP. However, rising freight and insurance costs, along with constrained refining capacity, are likely to keep prices elevated. We expect second-order effects of higher crude prices to weigh on inflation, demand, and manufacturing in the coming months.

With regard to valuation, the Nifty stock market is presently valued at 17 times its one-year forward earning multiple, which amounts to a 12.4% discount from its historical average of 19.4 times, which covers 15 years. In the base case scenario, it is assumed that the valuation will be 17.5 times, 10% discount from its historical average based on FY28 earnings per share (EPS) of 1,551, leading to a target price of 27,080.

Near-term corporate performance continues to be robust, with Q4FY26 seeing continued demand across all segments. Revenues, EBITDA, and profit before tax for the universe are projected to increase by 11.3%, 6.3%, and 5.7%, respectively. The segments that could contribute significantly to growth include automobiles, metals, telecom, NBFCs, healthcare, and construction. Meanwhile, other segments like consumption, IT services, and media are expected to deliver stable double-digit growth. Nevertheless, the pressure on margins is increasing, with input prices going up and most segments registering lower profits.

Domestic demand continues to hold steady, backed by the resilience of the rural sector and improving urban demand. Rationalization of GST, past quarters' low inflation levels, and stable interest rates have contributed to the recovery of consumption trends. Nevertheless, second-round effects, including higher crude prices, inflation, and adverse weather impacts, could constrain future demand trends.

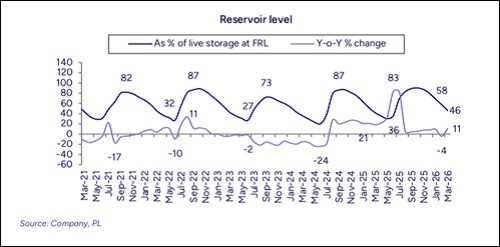

Skymet and other weather agencies have indicated the likelihood of an El Niño in the upcoming monsoon season, with rainfall expected to be below normal at 94% of the Long Period Average. The forecast points to a gradual weakening of monsoon activity through the season and a heightened risk of drought in parts of North, West, and Central India. From an economic perspective, this raises concerns around kharif output, reservoir levels, food inflation, and rural demand.

Capital expenditure will continue to be one of the major drivers of growth, with investments likely to continue coming through in defense, data centers, high-speed rail lines, renewables, and manufacturing clusters. Orders are coming in thick for capital goods as well as defense due to the push by the government for the same, especially in the latter, due to the tense geopolitical situation.

The banking sector is witnessing a recovery in credit growth, as it is now at around 14.3% on account of MSMEs, Vehicle loans, and NBFCs. On the other hand, inflation along with reduced liquidity levels can be restrictive factors for margins. The gap between repo rates and yields on government securities signifies that monetary conditions are rather tight.

Mr. Amnish Aggarwal, Co- Head Institutional Equities, PL Capital said, “Geopolitical tensions along with the sharp increase in oil prices have made the global macroeconomic environment highly uncertain. Though India’s growth fundamentals look intact in the longer term, near-term challenges related to inflation, interest rate concerns, and foreign demand are likely to impact economic growth. The current market valuations are already considering these headwinds, but any sustained turbulence may result in further earnings downgrades. Nonetheless, favourable domestic factors like increased investments in infrastructure, industrial production, and stability in the banking system are likely to underpin sustainable growth”

From a sectoral perspective, the approach continues to be positive for capital goods, defense, healthcare, banking, telecom, and metals, supported by robust order books, domestic demand, and favourable trends. Sectors that are oriented towards domestic consumption, including power utilities, NBFCs, jewellery, and pharma, are also likely to outperform. Nevertheless, caution needs to be exercised in relation to IT services, export-dependent sectors, cement, chemicals, and oil & gas, considering global risks and margins.

While India continues to have a good growth story ahead due to its strong domestic fundamentals, better infrastructure, and the development of the manufacturing environment, there are certain risks in the short term that need to be watched out for, including geopolitical risks, inflationary risks, impact of El Niño, and the overall slowdown in the global economy. In such a scenario, the new cycle would depend on how these risks balance out.

Above views are of the author and not of the website kindly read disclaimer