Financials Banking Sector Update : Growth momentum healthy; margin outlook divergent with negative bias by Motilal Oswal Financial Services Ltd

Asset quality remains robust

* Credit growth crosses 17% YoY; mid-sized private banks likely to lead: Systemic credit growth accelerated to 17.7% as of 15th Jun’26, driven by:

A) Higher working capital loan demand amid rising input costs

B) The regulatory shift in focus from LDR to the LCR/NSFR framework

C) A surge in corporate borrowings following the rise in bond yields during 1QFY27. We expect growth to likely moderate to around 14% by FY27E. The FCNR route should provide some relief and help deposits mobilization till Sep’26. Across our coverage, we expect banks to deliver loan growth of 1.2-5.4% QoQ in 1QFY27. PSU banks are likely to remain relatively subdued with less than 3% QoQ growth, while midsized private banks such as AU, RBL, DCB, and IDFC are expected to outperform with loan growth of 3.9-5.4% QoQ. Among the large private banks, we expect ICICI Bank to lead with around 4% QoQ loan growth.

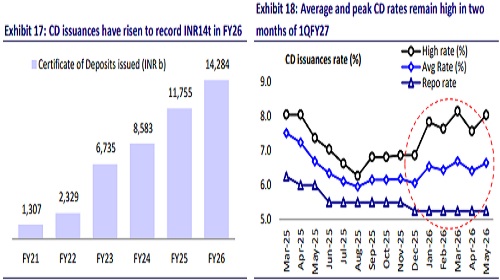

* Deposit growth at 12%; CD ratio rises to 83.4%: System-wide deposit growth remained healthy at 12% YoY, aided by strong credit expansion and an increase in the money multiplier. However, deposit growth continues to trail loan growth, resulting in greater reliance on wholesale deposits. With competition for deposits still intense, banks continue to face challenges in mobilizing lowcost deposits. We expect term deposit (TD) rates to remain broadly sticky as banks strive to sustain deposit accretion. Across our coverage universe (barring RBL), we expect deposit growth in the range of 0.5-5.1% QoQ.

* NIM outlook mixed; PSU bank margins likely to remain range-bound: With the repo rate being largely flat for the past six months, the external benchmarklinked loans have largely absorbed the full rate cut impact. Going forward, changes in product mix are likely to be the key driver of yield movements. In 1QFY27, a few banks have changed the deposit rates. Among mid-sized private banks, we expect NIM expansion for IIB, Federal (adjusted NIM) and DCB, while HDFC Bank, ICICI Bank and Axis Bank are likely to report a marginal decline and KMB to witness moderation. Among other PVBs, we expect NIMs to decline by ~13bp QoQ for AU, 10bp QoQ for Bandhan and 14bp QoQ for Equitas SFB. For PSU banks, margins are likely to remain broadly stable in a narrow range.

* Asset quality outlook remains healthy: Most of the banks have indicated that stress is easing in unsecured loans (PL/CC), while MFI stress is trending close to normalization. Our channel checks suggest no immediate impact of the West Asia war, though we expect the rise in input costs and margin contraction to dent profit margins of underlying borrowers. Among our coverage banks, we expect steady credit costs for large PVBs and benign credit costs for PSU banks.

* Estimate ~15% PAT CAGR over FY26-28: For 1QFY27E, we estimate NII for our banking coverage universe to improve by 10.9% YoY/3.5% QoQ and PPoP to rise by 4% QoQ. We estimate private banks’ PAT to grow by 10.1% YoY/fall by 1.7% QoQ and PSU banks’ PAT to grow by 9% YoY/decline by 6.6% QoQ. For our coverage universe, we estimate PAT to grow by 9.6% YoY/fall by 4% QoQ. We estimate our coverage banks to deliver a 15% earnings CAGR over FY26-28.

Private Banks: 1Q earnings to grow 10.1% YoY/fall 1.7% QoQ (+20.3% in FY27E)

* For the private banks under our coverage, we estimate PPoP to decline by 8% YoY/rise by 5.1% QoQ, and PAT to grow by 10.1% YoY/fall by 1.7% QoQ in 1QFY27. We estimate ~20% earnings CAGR over FY26-28 for private banks.

* Estimate NII to grow 10.4% YoY/2.9% QoQ in 1QFY27. Among large private banks under our coverage, NII is estimated to grow by 8.5% YoY (up 3.1% QoQ) for HDFCB and 10.5% YoY (4.1% QoQ) for ICICIBC. AXISB’s NII is likely to grow by 10.6% YoY/3.7% QoQ, and Kotak at 10.1% YoY/1.5% QoQ.

* Interactions with most of the banks indicate a stable asset quality outlook; however, we closely monitor business loans and CVs amid concerns related to the West Asia conflict.

PSU Banks: NIMs range-bound; 1Q PAT to grow ~9% YoY/dip ~7% QoQ (7% growth in FY27E)

* We estimate PSU banks’ PAT to grow by 9% YoY (down 6.6% QoQ) in 1QFY27E, supported by range-bound NIMs and modest fee growth, which would be partly offset by some increase in treasury gains amid the fall in bond yields.

* NII is likely to grow by 11% YoY/4.2% QoQ. Treasury gains are expected to improve as bond yields have declined from the peak.

* Asset quality outlook stable: Asset quality outlook is stable for PSU banks, while the recoveries from the write-off pool are declining. We expect benign credit cost to continue for PSU banks.

* We estimate PSU banks to report an earnings CAGR of 9.6% over FY26-28

Small Finance Banks: negative bias in NIM; growth to remain healthy

* AUBANK is expected to report PAT growth of 29.3% YoY (down 9.7% QoQ) to INR7.5b amid NIM decline of 13bp QoQ to 5.83%. However, improving slippages outlook and easing in MFI stress should keep credit costs at ~0.9-1% of assets. NII is expected to increase by 32.8% YoY (5.2% QoQ).

* EQUITASB is estimated to report a decline in PAT to INR1.58b in 1QFY27, due to a decline in NIM (down 14bp QoQ to 7.15%). We expect credit costs to moderate. We expect loan growth to remain steady (at 27.2% YoY/3.4% QoQ), led by healthy growth in MFI as well as used VF.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...