Financial Banking Sector Update :MOFSL BFSI picks 4.0: Earnings, growth and valuations to drive sector performance by Motilal Oswal Financial Services Ltd

Large private banks looking attractive; prefer stock-specific approach

* Banking stocks have delivered a mixed performance in the past one year, with midsized banks faring better and large private banks delivering a muted performance, dragged down by uncertain macro, margin pressure and persistent FII selling.

* The Nifty Private Bank Index was flat in the past 12 months as large-cap banks such as HDFCB, ICICIBC and KMB delivered negative returns of -18.9%, -6.5%, and -4.7%, respectively. Mid-sized private banks, including RBL Bank, Federal, SIB, CUB, and KVB, led the pack with returns of 70%, 56%, 58%, 40% and 42%, respectively.

* We maintain a balanced view as we expect the banking sector’s performance to improve going ahead, with improving macro and impending recovery in earnings. Additionally, management commentary is turning constructive, which, coupled with healthy credit growth, will boost investor sentiment.

* The model portfolio has navigated a volatile macro backdrop – tariff disruptions, geopolitical tensions, crude spikes, and currency pressures – leading to episodic drawdowns in BFSI stocks via NIM pressure, treasury MTM impact, and FII-driven sentiment, even as fundamentals remain stable. Despite this, our portfolio returns since inception at ~25% (details inside) have outperformed the Nifty Financial index and the Nifty-50 Index returns of 10% and ~5%, respectively, over the similar period.

* We continue to follow an active stock selection approach on the bottom-up basis and refresh our list of top-16 BFSI stocks from our overall BFSI coverage of >75 BFSI stocks. Please refer to Exhibits 1 and 3 for details on MOFSL BFSI picks 4.0 and the overall performance. We summarize our thoughts on various BFSI segments and preferred ideas below

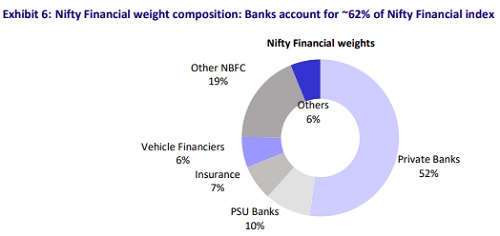

Banks: Growth outlook steady; NIMs to stabilize after persistent decline

* Banking system loan growth was robust at 17.6%, led by broad-based momentum across Corporate, Retail and MSME credit. This has been supported by healthy growth in working capital loans and demand substitution from bond issuances to corporate loans as bond yields have increased significantly. We estimate a 14% CAGR in banking system credit over FY26-28.

* Sector earnings growth has gained momentum, with earnings expected to post a ~15% CAGR over FY26-28E after a relatively subdued FY26 (6.6% growth). Banks have witnessed a modest decline in NIMs in FY26, driven by lower CoF, while loan growth was healthy. Additionally, easing asset quality stress in the unsecured segment will lower the credit cost for many mid-sized banks.

* With inflation on the uptick, the possibility of a rate hike during 2HFY27 has increased. Large private banks have a better NIMs outlook than PSBs owing to their higher mix of repo-linked loans. Over FY26-28, we estimate private banks to report a higher earnings CAGR of ~21% vs. an ~8% CAGR for PSU banks. For our banking coverage universe, we estimate a 15% earnings CAGR over FY26-28.

Private Banks: Business momentum healthy; earnings growth to gain pace

* For private banks, business momentum has been healthy and NIMs have largely bottomed out. A potential rate hikes in 2HFY27 will support margins. Unsecured loans saw growth revival, with MFI disbursements improving and banks looking to expand their PL and CC businesses in FY27.

* In the near term, NIMs are expected to remain stable, aided by stable CoF, which will be partly offset by slightly higher growth in corporate lending.

* Stress in unsecured retail MSME has eased, but potential challenges emerge in segments like CVs and M-LAP amid the ongoing West Asia conflict. We remain watchful and prefer large private banks with more diversified portfolios. Among large banks, we expect credit cost to remain under control, with AXSB reporting a 20bp decline in FY27E.

* We expect private banks to report an earnings CAGR of ~21% over FY26-28, supported by a stronger recovery for mid-sized private banks as unsecured portfolio stress eases, enabling a decline in credit cost.

* Preferred Buys: ICICIBC, HDFCB, SBIN, and AUBANK.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...