Financial Banking Sector Update :Banking system well poised for sustainable growth by Motilal Oswal Financial Services Ltd

Asset quality robust; strong underwriting + governance to aid continuity We met with the IBA Chief, Mr. Atul Kumar Goel, to discuss the outlook for the banking sector, including recent concerns around liquidity, profitability trends, and growth prospects, along with other key developments shaping the industry. The following are the key takeaways from our discussion

Credit opportunity intact; focus shifting to absolute NII growth

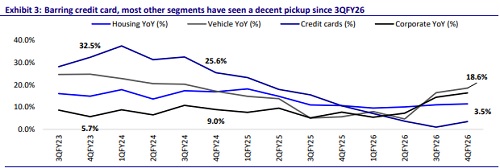

* While earnings growth across the sector has moderated from peak levels, the long-term credit opportunity is intact. Banks are shifting their focus to absolute NII growth rather than NIM expansion. India's economic growth trajectory continues to create significant credit demand opportunities across multiple emerging sectors.

* Key growth areas include renewable energy, electric vehicles, semiconductors, infrastructure, and other strategically important sectors. Mr. Goel believes there is substantial headroom for incremental credit expansion across the economy. Within the retail and MSME segments, pricing remains favorable, with MSME loans typically carrying a higher spread than comparable corporate loans, supporting profitability while serving as an important economic function.

CD ratio manageable; capital, borrowings, securitization and healthy profitability provide additional growth levers

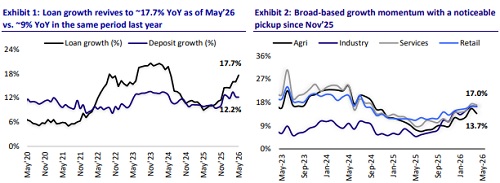

The banking system's CD ratio of ~82.7% should not be viewed solely through the lens of deposit growth. Banks have multiple avenues available to support balance sheet expansion, including capital mobilization, market borrowings, securitization transactions and healthy profitability levels. While deposits remain an important funding source, these alternate channels provide flexibility in supporting credit growth, particularly during periods when deposit mobilization trails loan growth. The recently announced FCNR (B) and ECB measures will also enable banks to raise resources at competitive rates, thereby supporting business growth. The growing sophistication of funding markets and securitization structures allows banks to optimize balance sheet utilization more effectively. As a result, the current CD ratio does not pose a structural constraint to future banking system growth.

Digitization and financial inclusion continue to deepen banking penetration

Recent discussions around deposits have focused on taxation-related aspects, including the marginal tax rate impact on savers. However, deposit mobilization should not be viewed in isolation, as the banking ecosystem continues to progress on multiple fronts, thereby increasing formal financial participation. Schemes such as Mudra and ECLGS have contributed meaningfully to credit penetration, while the rapid growth of digital payments has accelerated financial inclusion. India's payments ecosystem continues to witness strong adoption, with UPI processing approximately 24 billion transactions monthly and transaction values approaching INR29t per month. The increasing digitization of financial transactions is deepening customer engagement and creating opportunities for banks to expand product penetration across retail and MSME segments.

Gold loans remain attractive; digitalization improving customer acquisition

Gold lending remains a structurally attractive product category for banks. While regulatory guidelines permit LTV ratios of up to 85%, most banks currently operate closer to 50-70% on outstanding LTV basis, providing a meaningful cushion from a risk-management perspective. The key operational considerations in gold lending remain ensuring gold purity and maintaining robust storage infrastructure. Gold loans continue to function largely as an over-the-counter product, although the increasing levels of digitalization are improving customer acquisition and lead generation capabilities. Given its collateral-backed structure and strong customer acceptance, gold lending is expected to remain an important growth driver for retail banking portfolios.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...