Equity Outlook by Christy Mathai, Fund Manager- Equity, Quantum Mutual Fund

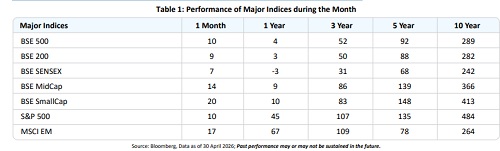

Markets rebounded sharply from the lows of March after announcement of ceasefire. Following table shows the change in broad market cap indices. On the global front, the US (S&P 500 Index) & Emerging Market Index had a similar rebound.

Earnings Trends amidst the ongoing West Asia Crisis

• FY2026 started with expectation of EPS improvement for major indices on the base of weak 2024/25. West Asia crisis has caused significant increase in key input raw materials along with increase in logistics costs. Sectors which are more susceptible to EPS cuts are OMC, select Utilities consumer discretionary and Materials. There could be further second order impact if the commodities prices remain elevated for longer.

• On the backdrop of West Asia Crisis companies started reporting their 4q26 numbers. Of the companies that have reported their numbers so far; performance remains a mixed bag. This might weaken further as we progress through the year in the context of elevated commodity prices.

Key trends are:

* Most of the Banks reported pickup in credit demand driven by SME and corporate book. Margin has stabilized as bulk of the loan book repricing is in numbers; elevated deposit rates will keep a check on margin expansion. Asset quality continues to be benign and West Asia crisis may normalize this number, higher. We largely remain positive on this pack; given the improvement in growth and undemanding valuations.

* IT Services companies have reported weak trends. The forward guidance has moderated owing to continued macro uncertainty and pricing pressures. On the positive side, deal wins continue to be strong. We find valuation in this pocket reasonable and remain optimist on recovery.

* Insurance: GST ITC (input tax credit) and other regulatory changes continue to weigh on company results in the near term. Companies are focusing on improving product mix and margins. General insurers witnessed improvement in operating parameters. We view this sector favorably as some of the large players have significant advantage in terms of distribution and scale; with good runway for growth.

* Cement: Sector witnessed improvements in EBITDA per ton driven by better pricing. Volume growth also remains healthy. Some of the input costs such as pet coke, coal, packaging material have moved up; which will impact term profitability. The industry is trying to pass on part of cost increase through price hikes.

Flows

DII (Domestic Institutional Investors) inflows at USD 5.0bn have outpaced FPI (Foreign Portfolio Investors) outflows at -USD 4.1bn. Higher crude prices along with pressure on capital inflows could pose pressure on currency. A weakening currency along with persistent global uncertainties would have a bearing on FPI flows.

What should an Investor Do?

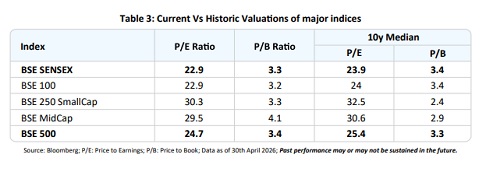

Though near-term earnings trend is linked to global developments, valuations have become conducive in many pockets (Refer Table 3). While short-term disruptions would have a bearing on near-term market movements, the impact on the intrinsic value of companies would be limited. Investors may consider staggered allocation to equities to take advantage of favorable valuations and benefit from the near-term potential volatility.

Above views are of the author and not of the website kindly read disclaimer