Economy Update : Oil imports rise but gold imports fall; FY27E CAD/GDP at 2.3% by Emkay Global Financial Services Ltd

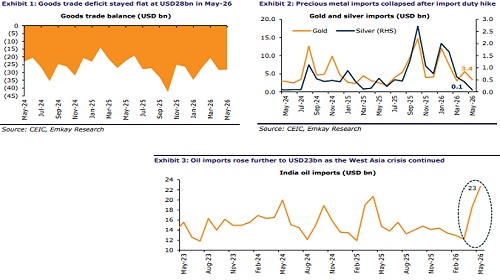

Goods trade deficit was nearly unchanged in May-26 at USD28.2bn (Apr-26: USD28.4bn), with oil imports rising 22% MoM (USD23bn). With prices remaining largely flat in May-26, crude and product import volumes are likely to have increased on a MoM basis. Gold and silver imports fell sharply (~39% and ~82% MoM, respectively) following import duty hikes during the month. Total imports rose 2% MoM to USD73bn, while total exports rose ~4% MoM to USD45bn. Oil exports dipped 12% MoM to USD8bn with higher export taxes on refined products. On the services front, net exports fell to USD17.7bn (with Apr-26 being revised downwards significantly); however, growth remained healthy. We maintain FY27E CAD/GDP at 2.3%, assuming average Brent at USD90/bbl. Despite the US-Iran deal announcement, physical oil market imbalances are likely to pose risks to oil prices moving lower in the short term. However, prices should correct meaningfully beyond 1HFY27, approaching USD70/bbl by end-FY27.

Goods deficit largely unchanged; oil imports rise, while gold+silver imports crash

Goods trade deficit was nearly unchanged in May-26, at USD28.2bn (vs USD28.4bn in Apr26), and was higher than estimate (Emkay: USD27.4bn). Imports rose 2% MoM to USD73.4bn, led by higher oil imports (USD22.7bn; 22% MoM) as the West Asia crisis persisted. Exports rose ~4% MoM to USD45.2bn. Crude oil and product import volumes increased by 4% and 8%, respectively, in April; a similar rise is likely to have occurred in May, given that oil prices remained largely flat. Oil exports fell ~12% MoM to USD8.4bn, likely reflecting the effect of higher taxes on refined product exports. Gold imports declined ~39% MoM to USD3.4bn, while silver imports fell even more sharply (~82% MoM; USD0.1bn), after import duties were hiked in May to 15% (from 6% earlier). Imports from Russia (29% MoM) and Oman (30% MoM) were sharply higher, likely reflecting diversification in energy import sourcing. Exports to the US rose 4% MoM to USD8.8bn, with momentum continuing following the lower US global headline tariff of 10%.

Core deficit moderates as core exports improve; YoY trends remain healthy

Core (non-oil, non-precious metals) exports rose 8% MoM (12% YoY) to USD34bn, while core imports were flat MoM (10% YoY) at USD47bn. As a result, core deficit dipped to USD13bn. Electronics goods exports slowed slightly (-2% MoM) to USD5.1bn but remained strong on a YoY basis (11%). Electronics goods imports also declined (-4% MoM) to USD12.3bn. Other major core export categories (drugs and pharma, chemicals) showed mixed momentum, while YoY growth remained healthy. Core export growth has remained below core import growth over the past six months, despite both product and geographical diversification.

Services surplus declines marginally in May; robust growth continues

Services surplus declined to USD17.7bn in May-26 (~12% YoY), with the Apr-26 surplus being revised down to USD18.6bn from USD21bn. As a result, provisional net services exports for FY27TD were at ~USD36bn, up ~15% YoY, with gross services exports (USD74bn) rising ~13%. For May-26, exports (USD36.8bn) rose 13% YoY, while imports (USD19.1bn) were up ~14% YoY. Net services exports have been resilient in CY26 despite numerous headwinds (AI, West Asia crisis etc) and have been helped by GCCs.

FY27E CAD/GDP maintained at 2.3%; short-term risks to lower oil prices

We expect both CAB and BoP to worsen in Q1FY27, with CAD/GDP at 0.5% (4QFY26: 0.7% surplus), led by a higher goods trade deficit and moderation in remittances and net services exports. We maintain FY27E CAD/GDP at 2.3%, with our Brent average forecast at USD90/bbl. Even with a US-Iran deal and SoH opening being announced, physical market imbalances are likely to pose risks to lower oil prices in the short term (Refer to: “Oil reality check: Why a deal may not be enough”). However, prices should correct meaningfully and sustainably beyond 1HFY27, with an oil supply glut materializing and taking prices to USD70/bbl by end-FY27.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354