CPI Inflation Eased to an All-Time Low of 0.3% in October by CareEdge Ratings

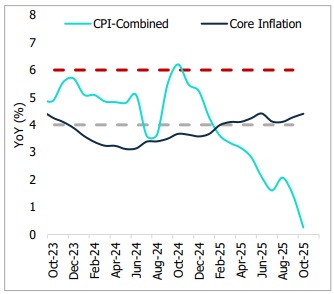

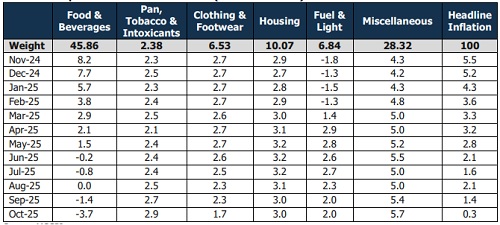

The CPI inflation continued to stay on a downward trajectory, easing to 0.3% in October 2025. The positive impact of the GST rationalisation and deflation in the food and beverages category supported the lower inflation print. Deflation in the food basket deepened further to 3.7% in October, from 1.4% the previous month. A further acceleration in the already double-digit inflation seen in precious metals pushed up the core CPI inflation to 4.4% in October. Excluding precious metals, core CPI inflation was seen at a benign 2.5%.

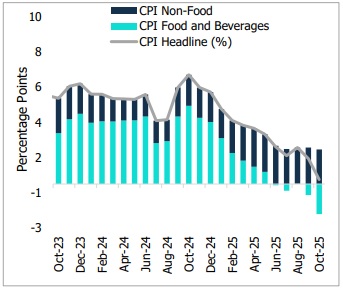

Within the food basket, deflation widened in items such as vegetables (-27.6% YoY), pulses (-16.2%), and spices (-3.3%). While inflation in edible oils witnessed some moderation, it continued to record double-digit inflation at 11.2% capping a further downside in overall food inflation. This trend remains a critical monitorable, particularly as global vegetable oil prices remain elevated, as reflected in the FAO Global Vegetable Oil Price Index, which rose 10.9% YoY in October. Furthermore, Kharif sowing of oilseeds has also been subdued, seen lower by 5.3% this year, which could extend inflationary pressures in this category. Overall, the price pressures in this category remain a monitorable given the weak sowing trends, import dependence, and elevated global edible oil prices. Nevertheless, the government's reduction in basic customs duty on imported edible oils and recent GST rate cuts on certain edible fats should help cushion the price pressures in this category. Among other components of the food basket, inflation in fruits moderated to 6.7% in October from 9.8% in the previous month. Overall, we expect food inflation to remain at moderate levels, supported by healthy agricultural activity and a favourable base. Furthermore, adequate reservoir levels and strong kharif sowing bode well for food price stability. However, the late withdrawal of the monsoon and crop damage amid heavy rains in certain regions pose some risk. On the external front, global commodity prices are expected to remain broadly benign, given weak global growth prospects, overcapacity in China, and OPEC’s decision to raise crude oil output.

Exhibit 1: CPI and Core Inflation

Exhibit 2: Contribution to CPI Inflation

Table 1: Component-Wise Retail Inflation (Year-on-Year %)

Way Forward

With the GST rate rationalisation rolled out towards the end of September, its positive impact was reflected in October’s lower inflation reading. Going forward, inflation is projected to average 0.9% in Q3 before rising to 3.1% in Q4 FY26. With food inflation subdued, we project an average inflation rate of 2.1% for FY26. From a monetary policy perspective, moderating inflation provides the RBI with greater room to focus on supporting economic growth amid continued external headwinds and uncertainties surrounding the trade negotiations with the US. If growth weakens in H2 FY26, the latest inflation readings could create scope for a rate cut.

Above views are of the author and not of the website kindly read disclaimer