India GDP :Growth surprises yet again; FY26E raised to 7.3% by Emkay Global Financial Services Ltd

2Q real GDP growth at 8.2% was a positive surprise, led by i) statistically favorable deflator effects (nominal GDP: 8.7%), ii) lagged effects of monetary and regulatory easing, iii) possible improvement in real purchasing power/consumption, and iv) limited hit so far on India’s exports (5.6% growth) amid frontloading/early trends of diversification, also helping clock steady manufacturing growth (9.1%) in 2Q. Growth was led by Services (mainly Financial and RE as well as Public admin/Defense), while industry growth saw a pick-up, led by manufacturing (helped by lower input costs as well). Private consumption improved, while government consumption saw negative growth amid controlled revex by the government in 2H. GFCF growth remained strong, likely led by public capex. The consumption revival is expected to gather pace in 2H on the back of higher real incomes and the GST reset; based on this along with some of the current dynamics continuing, we raise FY26E GDP growth to 7.3% – much higher than our earlier estimate (6.5%) as well as the RBI forecast (6.8%). Though 2H growth is likely to slow to ~6.7% (vs 1H: 8%), a US-India trade deal would improve the growth outlook. Nevertheless, nominal GDP growth will remain sub-8%, and slippage here will require recalibration of all macro and market variables.

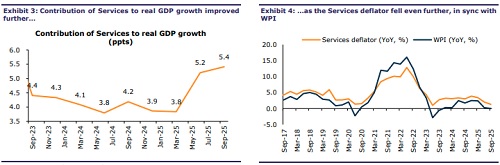

2QFY26 GDP/GVA growth at 8.2%/8.1%; nominal GDP growth at 8.7% Real GDP growth surged to an 18-month high of 8.2% in 2QFY26 (Emkay: 7.4%, prior: 7.8%), with a huge statistical boost due to a soft deflator of only 0.5%. Nominal GDP growth was 8.7% (prior: 8.8%). GVA growth at 8.1% (prior: 7.6%) was led by strong growth in the Services sector (9.2%), which was also helped by the deflator boost (which uses WPI as a proxy in the absence of PPI services). While Financial and RE rose 10.2%, Trade, Hotels, and Transportation slowed slightly to 7.4%. Public Admin/Defense and ‘Others’ growth stayed strong at 9.7%; albeit, this was at odds with general government fiscal data, which indicated lower growth in government spend in 2Q – this indicates that ‘others’ likely grew much faster. YoY Industry growth picked up (7.7% vs 6.3%), led by manufacturing (9.1%), likely reflecting frontloaded exports to the US ahead of the tariff deadline, as well as lower input costs. Agri growth was steady at 3.5%.

Expenditure – Led by private consumption, while investment steady Consumption led the show on the expenditure front, with private consumption improving to 7.9% (vs 7% prior), even as government consumption declined 2.7% amid slower government revex in 2Q (general government ex-interest revex growth fell 2.7% YoY in 2Q vs ~10% growth in 1Q). GFCF was healthy at 7.3% (7.9% prior) and likely led by healthy public capex (Centre+States’ growth: ~22% in 2Q). Export growth dropped to 5.6% and, with imports seeing further pickup (~13%), net exports continued to drag on the growth front.

FY26E raised to 7.3%; 2H growth to slow to ~6.7%, though tailwinds hover Going ahead, some of these dynamics will spill into 3Q as well, along with an improvement in consumer demand in the latter half of FY26 – this leads us to raise FY26E real GDP growth to 7.3%. This is significantly higher than our earlier estimate of 6.5% as well as the RBI’s current forecast of 6.8%, partly led by 1H data surprises. That said, 2H growth is likely to slow to ~6.7% vs 8% in 1H. Along with a sustained consumption revival (boosted by higher real incomes and the GST reset), growth could improve in 2H if a USIndia trade/tariff deal materializes; this would boost export growth. Further, lagged impact of monetary, fiscal, and regulatory easing could also help improve growth outcomes, while a pick-up in private capex following the consumption revival would benefit. However, FY26E nominal GDP growth is likely to still be sub-8% (FY25: 9.8%), with FY26E headline CPI at ~2% (and WPI likely to be sub-1%). This implies that all macro and market variables— fiscal deficit/GDP, sovereign debt/GDP, credit growth, corporate earnings, FPI flows, etc— will need to be recalibrated accordingly. Any slippage on nominal growth would imply much higher compression of fiscal deficit to achieve similar debt/GDP outcomes.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354