Cement Sector Update : Demand growth and profitability recovery expected in 2HFY27 by Motilal Oswal Financial Services Ltd

Cost relief emerging; but pricing power missing

Cement demand has largely been led by the infrastructure segment, while demand from the trade channel and rural markets remains relatively modest. We estimate industry volume growth of ~5-6% YoY in 1QFY27. Cement price growth remained modest in the past couple of years due to higher competitive intensity and low industry capacity utilization in the range of ~65-70% (over FY19-26). We believe the price hike to be gradual due to higher competitive intensity. On the other side, petcoke prices, which remained high during AprMar’26, have seen some moderation (down ~10-12% MoM in Jun’26 MTD). With recent correction in crude prices, we expect a further reduction in petcoke prices, which will provide relief from high variable costs in 2HFY27E. Capacity addition is significant in absolute terms, and are being planned aggressively by industry players, driving steady supply growth. We estimate that industry average grinding capacity utilization peaked at ~72% in FY24 and is expected to remain range-bound at ~70-71% over FY25-28E. We continue to prefer names with a track record of strong execution, volume growth, a favorable regional mix, improving cost matrix and higher return ratios. We are selective in our top picks in the cement space and prefer UTCEM and JKCE

Infrastructure driving cement demand growth

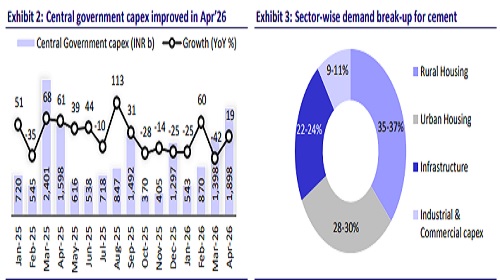

* Cement demand has largely been supported by infrastructure and institutional projects, which continue to account for a rising share of cement consumption. Central government capex, state infrastructure projects, data centers, industrial capex, warehousing, renewable energy installations, and urban development initiatives remain key growth drivers. Demand from large contractors and project business has been significantly better than retail channels, indicating that the recovery is currently investment-led rather than consumption-led.

* Trade demand in Tier-3 and Tier-4 cities, along with rural markets, remains relatively modest. Housing activity in smaller towns has not accelerated meaningfully due to uneven agricultural income growth and lingering liquidity challenges among rural consumers. Consequently, the retail segment is growing at a slower pace than infrastructure-linked demand.

* Regional trends continue to diverge. In 1QFY27E, the North and Central regions have seen the strongest momentum, benefiting from robust infrastructure execution and healthy construction activity. In contrast, certain pockets of the South, East and West regions saw weaker demand in 1QFY27E due to temporary disruptions from state elections and labor migration. Given these regional variances, industry demand growth in 1QFY27 is estimated at ~5-6% YoY.

* Looking ahead, demand will mainly depend on monsoon behavior. Expectations of lower rainfall remain a key risk. A deficient monsoon could hurt agricultural incomes, rural construction activity and housing demand in small towns, thereby delaying the recovery of the trade segment. Nevertheless, infrastructure-led demand may remain resilient given the government’s continued focus on capex. Over FY25/FY26, cement demand in the first half remained sluggish due to multiple reasons; however, it recovered strongly in the second half. We estimate a healthy recovery in cement demand in 2HFY27 as well, and estimate industry demand growth at ~6-7% YoY in FY27, following a healthy base of FY26

Valuation and view: Preferred picks remain UTCEM and JKCE

* Cement stocks have seen a steep correction in stock prices in Mar’26 due to the concerns around weak profitability, led by high input costs and sluggish price hikes, and overall slowdown in economic growth amid the West Asia crisis. However, with a recovery in the broader index, our coverage stocks have seen a mixed performance on YTDFY27. While a few stocks (BCORP, ICEM and JSWC) have outperformed the broader index (Nifty-50), some (DALBHARA, TRCL, and UTCEM) have underperformed. The remaining stocks (ACEM, ACC, JKCE, JKLC, and SRCM) were largely in line with the broader index performance.

* The sector currently trades at 1-year forward EV/EBITDA of 15.0x, at ~6%/19% discount to its 10-year/5-years average valuation. Meanwhile, industry ROCE bottomed out in FY25 at ~5% (due to lower profitability and higher capex). ROCE has improved in FY26, led by improvement in profitability. ROCE is estimated to remain range-bound over FY27-28 given the excessive supply against demand. With fuel costs coming down and demand trends improving, the risk-reward profile has become increasingly favorable from a one-year perspective.

* We continue to prefer names with a track record of strong execution, volume growth, a favorable regional mix, improving cost matrix and higher return ratios. We are selective in our top picks in the cement space and prefer UTCEM and JKCE.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...