Buy Yatharth Hospitals Ltd for Target Rs.1,050 by Choice Institutional Equities

We visited YATHARTH’s newly-commenced Model Town, New Delhi (300 beds capacity) and Sec-20, Faridabad (400 beds capacity) facilities and also met the Whole-time Director – Mr. Yatharth Tyagi, Mr. Ashutosh Kumar Jha (Group Chief – strategy, M&A and IR), Mr. Sunil Kapur (Head of Model Town facility) and Mr. Ajay Bharadwaj (Head of Sec-20 Faridabad facility). All the YATHARTH’s existing facilities are accredited by NABH. Model Town, New Delhi is a 300-bed hospital which began operations in July 2025. It currently operates at an ARPOB of over 40,000; its revenue being driven by Cash and TPA segments and zero reliance on govt business. Sec-20, Faridabad, is a 400-bedded hospital which began operations in September 2025. It currently operates at an ARPOB of over 36,000; its revenue being driven by Cash and TPA segments and nil reliance on govt business.

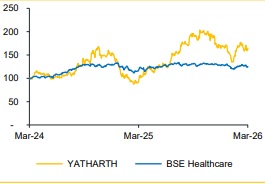

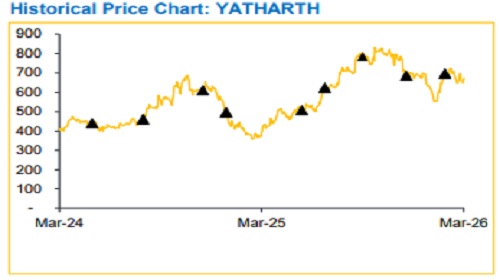

We remain confident that YATHARTH's growth trajectory will be sustained by its strategically targeted expansion across Delhi-NCR micro-markets, underpinned by a strong super-specialty portfolio. This approach is progressively driving higher ARPOB and improved margin, further cementing its position as a premier advanced tertiary-care hospital network in the region. We continue to expect to see a CAGR of 35.5%/35.7%/43.6% over FY25–FY28E and maintain our BUY rating with an unchanged TP of INR 1,050.

Key Takeaways from the Meeting

Operational Status

* The Faridabad facility is the second hospital in the city — having significant brand familiarity advantage versus entering a completely new market

* Model Town (Delhi) benefits from its proximity to existing NCR presence; offering a 'boutique' patient experience vs. high-volume competitors

Competitive Positioning

* Faridabad was previously lacking a corporately-run, large-scale hospital despite dense population. Nearest competitors are 150–250-bed facilities within its 10–15 minutes driving radius

* Model Town faces competition from listed hospital chains in the vicinity (Shalimar Bagh area) but stands out on superior infrastructure and a curated patient experience

Star Doctor Strategy: Each specialty at the new hospitals includes at least one physician who is recognised among the best doctors in Delhi-NCR.

Government vs. Private Mix

* Group-level government business at present is ~30–35% of revenue; target is to reduce to ~25% over the coming years • New hospitals (Faridabad, Model Town) intentionally capped their government business at 10–12%. This is due to higher ARPOB from private; critically, better debtor days and receivable cycles

* Government volume was previously used to drive occupancy; with star doctor-led private demand, this trade-off is no longer necessary at new facilities

Insurance Empanelment & Third-party Aggregators

* New hospitals can accept private insurance patients from Day 1 via Thirdparty Aggregators (TPAs), which offer cashless admissions and reimburse from patients later.

* The management has strong existing relationships in the private insurance sector, enabling faster empanelment timelines vs. industry peers.

Bed Count Growth

* Now targeting a doubling from the current base of ~2,550 beds in ~3 years

* Current 400-bed Faridabad hospital: ~50% of beds operational; ready to scale up floor-by-floor as census grows.

Oncology — Growth Vertical

* Medical and surgical oncology operational for sometime. Radiation oncology only began ~1.5 years ago at Noida Extension

* Group-level oncology contribution: ~10–11% of revenue at present

* Without radiation capability, oncology volume is constrained — patients prefer one-stop solutions (chemo + radiation at same facility)

Expansion Plans

* Radiation oncology to be launched at Faridabad hospital in ~6–7 months; Model Town in ~7–8 months

* Target oncology revenue mix for each new hospital individually: over 20% (vs. ~10% group average today)

* Group-level oncology mix target: Over 15% in 3 years (medical + surgical + radiation + bone marrow transplant).

Geographic Strategy & Future Markets

* Gurgaon flagged as a key target market, specifically newer corridors near Dwarka Expressway

* Agra is the first major expansion outside NCR; management comfortable with UP and Haryana but emphasises infrastructure quality as the non-negotiable filter

* 'First-mover advantage' in NCR micro-markets which are still underpenetrated remains a strategic priority

* Expansion outside established geographies (e.g., Gujarat) not in focus at present; political/regulatory risk and management bandwidth cited as reasons.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131