2025-10-15 05:42:15 pm | Source: Motilal Oswal Financial Services Ltd

Neutral United Breweries Ltd For Target Rs. 2,000 by Motilal Oswal Financial Services Ltd

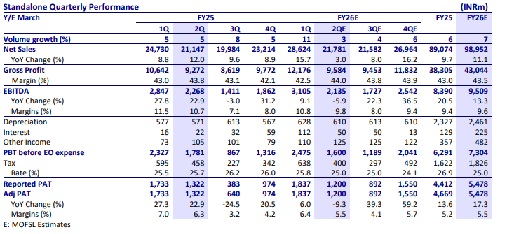

* We expect 3% revenue growth and 3% volume growth YoY, impacted by a weak summer and extended monsoon.

* UBBL continues to gain market share in premium segment; this should aid realization.

* GM will improve 10bp YoY to 44.0% on stable RM prices.

* EBITDA margin expected to contract 90bp YoY to 9.8%. UBBL continues to undertake various cost-saving initiatives, though weak demand to lead to operating deleverage.

* The outlook on state mix and realization growth remains a key monitorable.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

FM Nirmala Sitharaman addresses diaspora in France, ...

Trump's financial disclosure reveals 18 Coupang stoc...

The Eagle Eye : Geopolitical easing strengthens Indi...

26.35 crore verified APAAR IDs generated across India

Korean won falls nearly 6 pc against US dollar this ...

Minister Jyotiraditya M Scindia to lay foundation st...

Financials - Banking Sector Update : A quarter of di...

APEDA facilitates first export of J&K's premium cher...

Upgrade to Buy ONGC Ltd for the Target Rs 288 by Mot...

Centre and state government policies give fresh mome...