Neutral United Breweries Ltd for the Target Rs.1,425 by Motilal Oswal Financial Services Ltd

Weak performance; near-term pressure on margins

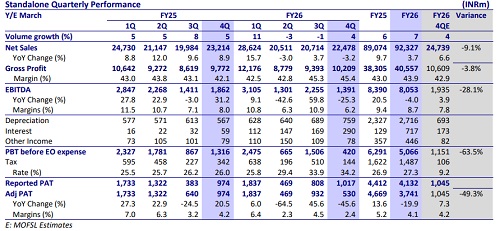

* United Breweries (UBBL) reported a 3% YoY decline in revenue (est. +7%, +4% in 3Q), despite 4% volume growth. Secondary volume growth was healthy at 8–9% YoY. Realization was down 7% because of a temporary higher mix of contract manufacturing. The premium portfolio delivered a healthy 16% volume growth (21% in FY26). Beer industry growth was ~10% at the consumer level, supported by favorable regulatory developments, improved affordability, and stable demand conditions.

* GM expanded 330bp YoY to 45.4% (est. 42.9%), aided by premiumization, pricing actions, and improved procurement efficiencies. Brand investments increased by ~27% YoY, ahead of the peak summer season. EBITDA contracted 180bp YoY to 6.2% (est. 7.8%). Such volatility in EBITDA margin has been witnessed in the previous quarters as well.

* The company indicated a cost pressure of INR 4–5bn amid ongoing geopolitical disruptions due to inflation in packaging materials, energy, and logistics. However, the company already expects to mitigate ~50% of this cost impact through productivity initiatives, selective pricing actions, and rationalization of trade spends in low-margin markets.

* Management expects high single-digit volume growth and double-digit revenue growth in FY27. Cost inflation will continue to impact GM; we build lower overhead costs driven by cost efficiencies, which will cover the RM cost pressure. We model a 9.5% EBITDA margin for FY27, but there can be downside risk in the margin if cost inflation sustains. Given rich valuations and lingering cost headwinds, we reiterate our Neutral rating on the stock with a TP of INR1,425 (premised on 50x Mar’28E EPS).

Miss on all fronts; the volatile quarterly trend continues

* Weak revenue; premium volumes up 16%: UBBL’s standalone net sales declined by 3% YoY to INR22.5b (est. INR24.7b) despite volume up by 4% (est. +4%). Secondary sales growth was at 8-9%; inventory correction impacted primary performance. The price mix performance was negative due to a higher mix of contract manufacturing. The Premium portfolio continues to grow strongly and posted 16% volume growth (+21% in FY26).

* Miss on operating margins: Gross margin expanded 330bp YoY to 45.4% (est. 43%). Other expenses were up 14%, while employee expenses inched up 2% YoY. EBITDA margin contracted 180bp YoY to 6.2% (est. 7.8%, 10.9% in 3QFY26).

* Dip in profitability: The EBITDA fell 25% YoY to INR1.4b (est. INR1.9b). Interest costs were up ~395% YoY to INR290m (est. INR173m). APAT dipped 46% YoY to INR530m (est. INR1,045m). There was an exceptional gain of INR740m in the quarter due to the transfer of freehold land.

* In FY26, net sales grew 4%, while EBITDA/APAT dipped 4%/20%.

Highlights from the management commentary

* The company highlighted that the beer category witnessed a strong recovery in 4Q, with ~10% growth. Growth was broad-based, with most markets contributing positively. Category growth was supported by regulatory developments, improved affordability, and stable demand conditions.

* Management indicated that the weak price-mix performance in the quarter is not structural, as it was hit by temporary factors such as inventory correction and higher reliance on contract manufacturing.

* Cost pressures remain elevated, driven by inflation in packaging materials, energy, and logistics, due to geopolitical disruptions (INR4-5bn impact). The company has already identified mitigation plans for ~50% cost increase (INR2.0- 2.5b) through productivity initiatives, selective pricing actions, and rationalization of trade spends in low-margin markets.

* The company expects high-single-digit volume growth in FY27, which will lead to double-digit revenue growth.

Valuation and view

* We cut our EPS estimates by 13-15% for FY27 and FY28 due to cost inflation and consistent delay in margin recovery.

* The beer industry is seeing a recovery supported by favorable regulatory developments, improved affordability, and stable demand conditions. A favorable policy environment remains a key growth driver, with no major tax hikes on beer across most recent state policies and relatively higher taxation on spirits improving beer affordability. Management is expecting the mid to high single-digit volume growth in FY27, which will lead to double-digit revenue growth.

* Management expects high single-digit volume growth and double-digit revenue growth in FY27. Cost inflation will continue to impact GM; we build lower overhead costs driven by cost efficiencies, which will cover the RM cost pressure. We model a 9.5% EBITDA margin for FY27, but there can be downside risk in the margin if cost inflation sustains. Given rich valuations and lingering cost headwinds, we reiterate our Neutral rating on the stock with a TP of INR1,425 (premised on 50x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412