Buy Triveni Turbine Ltd for the Target Rs. 620 by Motilal Oswal Financial Services Ltd

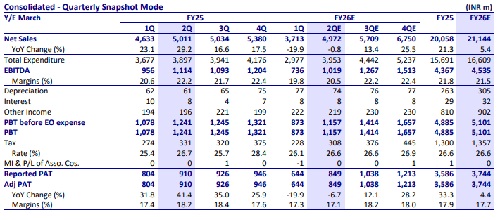

* Revenue is likely to grow on improved execution (vs. weak trends in 1QFY26), while delayed decision-making on international geographies may reflect in low order inflows. Domestic segment inflows are expected to grow QoQ.

* Key monitorables include a ramp-up in domestic and international inflows, conversion of inquiry pipeline and recovery of execution in 2H.

* We expect margins to decline YoY by 170bp, driven by revenue mix.

* Domestic ordering from the government and private sectors, updates on API turbines, and export order recovery will be the key areas to monitor.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412