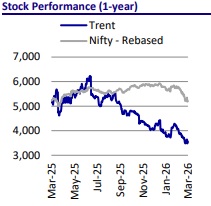

Buy Trent Ltd for the Target Rs.4,350 by Motilal Oswal Financial Services Ltd

.jpg)

Earnings downgrade cycle could continue in near term, to weigh on re-rating

* Trent’s revenue growth has decelerated over the past few quarters owing to weak LFL (in non-cluster stores) amid weak discretionary demand, rising competition in metro/tier 1 markets and its entry into lower-tier markets, which take time to reach desired productivity levels.

* Our recent channel checks indicate that cannibalization impact on existing stores is gradually easing, but the growth from reset base remains muted.

* Despite muted productivity and lower gross margin, cost efficiency measures led to ~110bp operating leverage in 9MFY26. However, we believe further margin expansion would depend on recovery in LFL growth.

* With Zudio undergoing the consolidation phase, TRENT might miss the expectations of ~200 net store additions in FY26 (~125 so far), which could lead to the continuation of earnings downgrades in the near term.

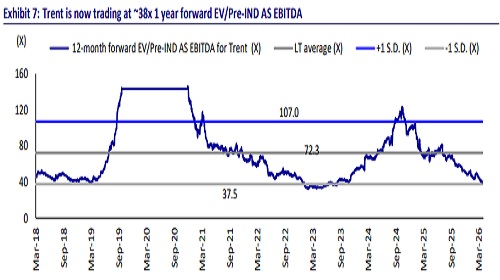

* After the recent correction, the stock now trades at ~32x FY28E pre-IND AS EBITDA (significantly below its past history but still at a premium to other Indian fashion retailers). We maintain our Buy rating with a revised TP of INR4,350 (earlier INR5,200), premised on ~40x FY28E pre-IND AS EBITDA.

Zudio undergoing consolidation; focus rising on tier 2+ towns

* Zudio scaled up aggressively from ~80 stores in FY20 to 765 by FY25 (at ~57% CAGR), driven by its strong value proposition, integrated supply chain and faster replenishment cycle.

* However, with rising base and driven by internal consolidation to strengthen the value proposition, the pace of store additions has moderated to ~125 stores in FY26TD. While store additions are traditionally skewed toward 4Q, we believe the company might miss the expectations of ~200 net store additions in FY26.

* In the past two years, Zudio has focused on expanding its presence to tier 2+ towns, with city presence rising to 265 in 9MFY26 (vs. 164 in FY24).

* Further, we note that the share of top seven states in incremental additions has been declining, with 37% net additions in 9MFY26 (vs. 60% in FY23-25).

* The new markets typically take more time to achieve the desired productivity, which weighs on overall company-level productivity (blended SPSF declined ~16% YoY in 9MFY26).

Westside expansion resumes after a pause with wider assortment

* Trent calibrated the pace of store additions in Westside (~48 net additions, ~7% CAGR over FY22-25) as it was focused on improving the brand’s customer proposition, along with product reimagination and select premiumization of its own brands (Utsa, Vark). The company has increased its focus on emerging categories and is ramping up its online presence.

* With the improved customer experience in line with the renewed brand proposition, the company consolidated lower-sized Westside stores into Zudio format while opening larger Westside stores (leading to avg. store area for Westside rising to ~22k sqft from ~16.5ksqft in FY21).

* With the renewed proposition, Trent has again accelerated the pace of Westside store additions in 9MFY26 (with 30 net additions or ~17% YoY).

* Further we note that its focus has shifted to deepening penetration beyond top seven states (~47% of 9MFY26 store additions vs. ~94% over FY22-25).

* Going ahead we build in modest ~20-25 annual store additions (~11% area CAGR over FY26-28E) in Westside, which could have upside risks.

Densification, rising competition and tier 2 forays hurt store productivity

* The company’s focus on increasing store density in select micro-markets has led to cannibalization of sales for existing stores and thereby store productivity (blended monthly SPSF down from ~INR1,247 in FY24 to INR1,125 in 9MFY26).

* Our recent channel checks indicate a gradual easing in the cannibalization impact, though sales growth from the reset base remains modest so far.

* With rising competitive intensity in metro/tier 1 markets and typically slower ramp-up and lower productivity in tier 2+ towns, we do not expect Trent’s blended store-level productivity to get back to super normal levels of FY23-24 in the near to medium term.

* As a gradual easing of the cannibalization impact gets offset by the rising presence in tier 2 markets, we build in a modest ~1-2% YoY reduction in store productivity over FY26-28.

Process efficiency-driven margin expansion largely in the base

* Despite near-term growth weakness and reduced store productivity, Trent’s profitability improvement has been structural.

* The pre-Ind AS EBITDA margins expanded from 9.3% in FY19 to 12.8% in FY25 (further to 13.7% in 9MFY26), led by process efficiencies and cost rationalization initiatives such as RFID-led manpower reduction, faster billing cycles, tighter inventory control, and a higher mix of variable rentals.

* Combined with a robust supply chain and backend infrastructure, TRENT delivered ~23% YoY growth in 9MFY26 pre-IND AS EBITDA (despite weaker 17.5% revenue growth vs. ~39% YoY area addition).

* However, with the benefits of RFID implementation on manpower costs largely in base, we believe the margin expansion going ahead would be driven by recovery in store productivity; hence, we model steady standalone pre-IND AS EBITDA margins over FY26-28 at ~13.2%.

Earnings downgrade cycle could continue in the near to medium term

* With Trent’s revenue growth decelerating, its consensus FY26 revenue/EBITDA/EPS estimates have been reduced by 11%/5%/16% and FY27 revenue/EBITDA/EPS estimates have been lowered by sharper 16%/11%/25% over the past 12 months.

* Interestingly, Trent’s FY27 EPS estimate was upgraded from INR74 at FY25 start to ~INR91 by 1HFY25. However, with revenue growth decelerating since then, the current FY27 consensus EPS estimate stands lower at INR61.

* Despite significant earnings downgrades, we note consensus FY27 EPS estimate is still ~7% ahead of our estimate and could see further downside risks from a) weaker-than-estimate Zudio store additions, and b) higher-than-expected impact from store cannibalization, competition and weaker productivity in lower tier cities.

Valuation and view

* Trent's growth rate has decelerated materially over the last few quarters due to weak LFL amid a subdued demand environment and self-cannibalization of existing stores to increase its revenue market share in select micro-markets.

* We believe the impact from cannibalization should gradually ease; however, store productivity is unlikely to get back to FY23-25 levels.

* Despite relatively weaker revenue growth, Trent continues to display strong cost controls (especially tech-led reduction in employee costs) and report healthy EBITDA growth.

* With RFID-led benefits largely in the base, SSSG recovery remains the key driver for further margin expansion. We build in stable pre-IND AS EBITDA margins at 13.2% over FY26-28, which could have downside risks if the SSSG trends remain muted.

* We have marginally fine-tuned our FY25-28 estimates. We build in a CAGR of 19%/19%/12% in standalone revenue/pre-IND AS EBITDA/adj. PAT over FY26- 28E, driven mainly by retail footprint additions (~20% CAGR). Our pre-IND AS EBITDA margin is stable at ~13% over FY26-28E.

* Reiterate BUY on Trent with a revised TP of INR4,350 (earlier INR5,200), premised on 40x FY28E EV/pre-IND AS EBITDA for the standalone (Westside and Zudio) business, 2x EV/sales for Star JV, and ~1.5x EV/EBITDA for Zara JV.

* After the recent correction, the stock now trades at ~32x FY28E pre-IND AS EBITDA and ~51x FY28 P/E, which is still at a significant premium to other Indian fashion retailers.

* We continue to like Trent for robust store economics of its retail formats, long runway for growth in Star (presence in just 11 cities), and potential scale-up of emerging categories (Beauty, Innerwear and Footwear). However, revenue growth acceleration remains a key trigger for a re-rating.

* Among our large-cap retail coverage universe, we prefer Lenskart, VMM, and DMart over Trent.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041