2025-07-15 11:17:40 am | Source: Motilal Oswal Financial Services Ltd

Buy Tata Consumer Products Ltd For Target Rs. 1,300 by Motilal Oswal Financial Services Ltd

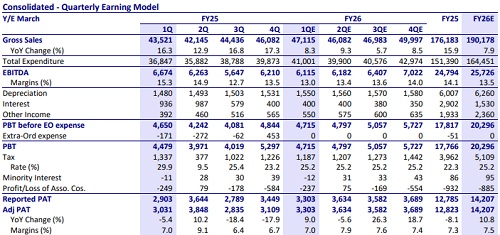

* We expect revenue to grow ~8% YoY, led by growth from domestic businesses.

* EBITDA margin is likely to contract to ~13% in 1QFY26 vs. 15.3% in 1QFY25.

* We expect tea volumes to grow at the same rate as 4QFY25 at ~4%.

* We expect the salt segment to witness a good quarter, driven by higher volumes and price hikes.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Indian Railways okays Rs 440 crore project for 3rd l...

Cipla clocks 39 pc drop in its Q1 profit, expenses u...

PM Narendra Modi's 3-nation visit reflects India's e...

Gurugram emerges as North India's first 100 million ...

Tamil Nadu records higher revenue in first quarter d...

Proposed US tariffs on generics could hit India's ph...

UltraTech Cement gains on getting nod to raise Rs 5,...

IndusInd Bank shares tumble over 6 pc after Q1 results

Indian economy navigates global uncertainties effect...

Indian banks report 146 pc surge in SMS scams

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...

Financials Banking Sector Update : Are there upside risks to FY27E credit growth by Motilal Oswal Financial Services Ltd

Consumer Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd

Automobiles Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd