Buy Supreme Industries Ltd for the Target Rs.4,200 by Motilal Oswal Financial Services Ltd

Healthy volume growth with an improving industry outlook

Operating performance below our estimates

* Despite lower-than-expected performance, Supreme Industries (SI) saw an improvement in its quarterly result, with an EBITDA growth of ~7% in 3QFY26 (vs. a dip in the last five quarters). The improvement was mainly driven by high overall volume growth of 13% YoY. Margins were flat YoY due to volatile PVC pricing in 3Q, offset by a better product mix. Plastic pipe volume rose ~16% YoY, with volume growth guidance maintained at ~15-17% for FY26. This implies a 20-24% YoY volume growth in 4Q.

* However, management cut its full-year margin guidance to 13.5-14.0% from 14.5-15.0% due to continuous PVC price erosion until Dec’25. Normal margins of 14.5-15.0% are expected to return once price volatility stabilizes and volumes scale up (expected in 4Q).

* Factoring in lower 3Q numbers (hit by muted margins, higher finance costs, lower other income, and reduced share of profits from JV), we cut our FY26E earnings by 9% while broadly retaining our FY27/FY28 estimates. We reiterate our BUY rating, valuing the stock at 34x FY28E EPS to arrive at our TP of INR4,200 (on par with its last 10-year average P/E valuation)

Margins under pressure amid pricing volatility

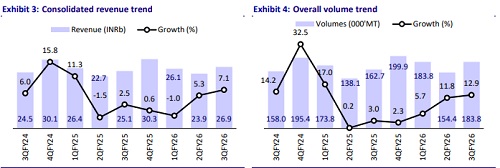

* Consolidated revenue grew 7% YoY to INR26.7b (in line), led by growth in volume (up 13% YoY) to 183.8k MT, which was offset by a decline in realization (down 5% YoY to INR146/kg).

* Consolidated adj. EBITDA rose 7% YoY to INR3.3b (est. INR3.6b), with an EBITDA margin of 12.3% (est. 13%), which remained flat YoY. EBITDA/kg for the quarter was INR17.9/kg (-6% YoY). EBITDA was adjusted for a onetime provision related to the new labor law, amounting to ~INR154m.

* Adj. PAT declined 12% YoY to INR1.6b (est. INR2.2b).

* Plastic piping products reported a volume of ~147k MT (+16% YoY). Revenue stood at INR18b (+10% YoY), and EBIT was INR1.4b (-2% YoY), resulting in an EBIT margin of 7.4% (-90bp YoY). Realization came in at INR124/kg (-6% YoY), while EBIT per kg stood at INR9.2/kg (-16% YoY).

* For industrial products, revenue was INR3.4b (flat YoY), EBIT was INR270m (-1% YoY), and EBIT margin stood at 8% (-10bp YoY). For packaging products, revenue was INR3.9b (-2% YoY), EBIT was INR334m (-24% YoY), and EBIT margin stood at 8.6% (-250bp YoY). For consumer products, revenue came in at INR1.1b (+5% YoY), EBIT was INR172m (+1% YoY), and EBIT margin stood at 15.3% (-60bp YoY).

* For 9MFY26, volume/revenue grew 10%/4% YoY to 522k MT/INR76.9b, while EBITDA/Adj PAT declined 7%/20% YoY to INR9.5b/INR5.4b. For 9MFY26, the company faced an inventory loss of INR1.0-1.2b.

Key highlights from the management commentary

* Valued Added products (VAP): VAP revenue grew 16% YoY to INR11.2b in 3Q, which boosted margins. The CPVC segment witnessed strong volume growth of 30% in 9MFY26.

* Plastic pipes: Plastic piping business growth is coming back to normalcy as the continuous downward price trend scenario has been arrested, and restocking has been started by channel partners. Polymer prices have moved up in CY26 (currently at ~USD650 vs. a low of USD580), broadly aided by an improvement in demand in the market. China's export restrictions starting from Apr’26 are expected to further drive prices up.

* Capex and expansion plans: Plastic piping segment capacity to reach 1mMT by the end of FY26, with 70% utilization expected in FY27. SI is spending capex of INR12b in FY26, including the Wavin acquisition. It is also planning to set up two more greenfield plants for plastic piping in Bihar and Alampur (combined capacity of ~100kTPA). This will be operational by FY28.

Valuation and view

* Macro headwinds affecting the PVC industry are largely behind, evidenced by PVC prices increasing from CY26 onwards and demand recovery resulting in double-digit volume growth for SI over the last two quarters and strong 4Q guidance. Margins are expected to improve, led by the omission of inventory losses, stable to improving PVC price expectations, an improving mix of VAP, and higher growth in the high-margin CPVC segment.

* We expect SI to clock 12%/18%/18% CAGR in revenue/EBITDA/PAT over FY25- 28. We value the stock at 34x FY28 EPS to arrive at a TP of INR4,200 (on par with its last 10-year average P/E valuation). Reiterate BUY.

* The one-year forward P/E valuations are at their 10-year historical average, and with an improving business performance and a healthy industry outlook over the next few quarters, we expect SI to provide a decent risk-reward.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041