Buy SAMHI Ltd for the Target Rs.200 by Choice Institutional Equities

West Asia Disruption Weighs on Q4; May 2026 fairs better

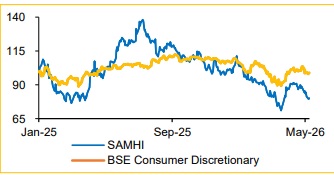

West Asia conflict continued to adversely impact SAMHI’s operating performance in Q4FY26; however, lower base in Q1FY26 has led to improvement in the upcoming quarter. Q4FY26 revenue grew 8.2% YoY, while RevPAR increased only 1.4% YoY. EBITDA margin for Q4FY26 was affected by softer demand, pushing ARR below the threshold of INR 7.5K. The margin was also hit by GSTrelated changes (~INR 140 Mn in H2FY26). Further, the margin was dented due to one-off pre-opening expenses and other cost. Growth visibility remains strong, supported by a robust pipeline including the near-term launch of WHyderabad in FY27E (170 keys) and stabilisation of SAMHI’s recentlyopened assets. The company’s focus on capital-efficient expansion, FCF generation and balance sheet deleveraging reinforces our thesis.

View and Valuation

We revise our FY27E/FY28E revenue estimate downwards by 3.1% / 4.7%, respectively, factoring in weaker inbound demand and delay in execution of one of the hotel assets. We lower our EBITDA margin estimate by ~1pp for FY27E/FY28E, incorporating margin pressure from GST-related changes and inflationary scenario. We believe SAMHI’s stronger balance sheet and stabilised cashflow will support incremental growth projects. Hence, we revise EV/Adj. EBITDA multiple to 10.0x for FY28E (vs. 9.0x earlier), arriving at a Target Price of INR 200 (maintained). Our DCF-derived valuation of INR 200/share provides a sanity check. We, therefore, maintain our ‘BUY’ rating on the stock, implying an upside of 36.1%.

Key Risk to our Valuation

Possibility of prolonged geopolitical disruption impacting inbound travel demand, probable execution delays/cost overruns across upcoming developments and incremental supply in key micro-markets.

West Asia Conflict Squeezes Margin despite RevPAR Gains

* Overall RevPAR grew by just 1.4% for this quarter, negatively impacted by geopolitical disruption

* Revenue grew 8.2% YoY to INR 3.5 Bn

* EBITDA decreased 9.5% YoY to INR 1.1 Bn, while margin declined 631 bps to 32.4%

* Reported Profit for the quarter came in at INR 4.0 Bn

OCF Generation to Fuel Key Growth, Further Deleveraging Expected SAMHI is targeting a robust owned hotel expansion pipeline across Hyderabad, Bengaluru, NCR and Chennai, with keys expected to expand at a 7.6% CAGR (FY26 –FY30E), while maintaining a capital-efficient strategy. We anticipate SAMHI to generate ~INR 600 Mn/year of cashflows, broadly sufficient to fund its planned capex pipeline of ~INR 11.4 Bn. Additionally, we forecast Net Debt/EBITDA to decrease from 3.5x in FY26 to 2.1x in FY28E. Long-term earnings’ growth is supported by upgrades of certain assets from Upscale to Upper Upscale and the acquisition of the experiential luxury brand ‘RARE India’.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)