Buy Rallis India Ltd For Target Rs.355 by Elara Capital

Turnaround efforts bearing fruit

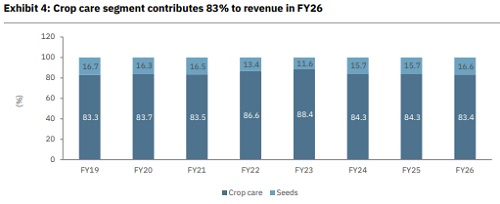

Rallis India (RALI IN) reported top-line growth of 6%, in line with our estimates, fueled by 5% volume gains and 1% price hike. Growth spanned all segments except B2B. Gross margin expanded, driven by the soil & plant health business, custom synthesis segment, and the seeds business. Crop protection business margin was steady amid liquidation of low-margin products.

Since Gyanendra Shukla’s appointment as MD & CEO, targeted efforts are on to revive its glory days – with results emerging and more to come. A strong H1FY27 agrochemicals season should accelerate superior earnings growth. We retain Buy with a higher TP of INR 355.

Normalcy creeping in raw materials availability: Post Iran-US war, there was a phase when the industry was facing force majeure from suppliers. That is now over, and normalcy is creeping in gradually. Materials are available; they may not be abundant, but supplies continue. Post war, the crop protection market has shifted from a buyer’s market to seller’s. Prices have increased by ~20-25%, as per management. RALI is adequately stocked for the Kharif season and does not want to buildup inventory within the company.

Seeds business is set to grow in the double digits: RALI’s strategy to drive scale and efficiency in the seeds business is focused on five crops: cotton, maize (corn), millets, mustard, and rice. We expect the seeds business to continue to grow in the double digits, driven by volume growth and realization leg-up. Cotton would continue to drive seeds business growth.

B2C business grows 15%, driven by legacy brands: Around 5% growth in the crop care business in Q4 was driven by 15% growth in the B2C business and 27% growth in the soil & plant health business. Legacy brands drove growth in the formulations space. RALI has launched two new insecticides brands: 1) ALSTOR – which is a combination of chlorantraniliprole and fipronil to control stem borer in paddy, and 2) FIPLAM – a patented combination of fipronil and lambda to control thrips, jassids and borers in cotton and horticulture crops, such as tomato, chilli, and onion. The B2B segment revenue declined 7%, due to lower volume.

Retain Buy with a higher TP of INR 355: While the Kharif season is likely to coincide with the El Nino phenomenon, we expect crop protection consumption to grow in India. Skymet’s monthly rainfall distribution forecast of 101%/95%/92%/89% of LPA for June/July/August/ September shows volatility in-between the Monsoon months is likely to be lower. Similarly, State-wise rainfall distribution forecast data does not indicate acute shortage in any of the agriculturally important states. Hence, we expect RALI to deliver healthy top-line growth and profitability. We increase our profitability assumptions for the seeds business, which has led to EBITDA growth of 7% for FY27E and 2% for FY28E. We introduce FY29 estimates. We retain Buy with a higher TP of INR 355 from INR 313 based on 20x (unchanged) FY28E EPS of INR 17.8.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

.jpg)