Buy Maruti Suzuki India Ltd for the Target Rs.15,200 by Choice Broking Ltd

View and Valuation:

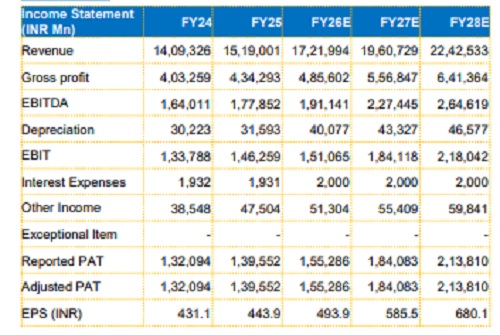

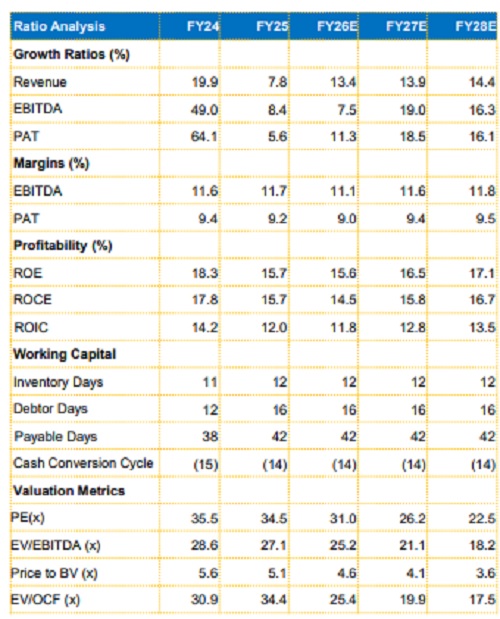

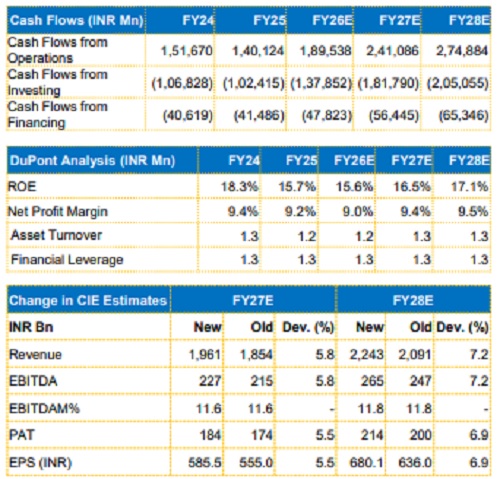

The entry level car segment which has seen a decline over the past few years can see a stimulus due to the GST rate cuts, making it more accessible for the first time buyers and middle income families. MSIL, being the largest manufacturer of passenger cars, stands to gain most from the GST rate cut for the small car segment. Around 80% of MSIL’s portfolio is set to benefit due to these rate cuts. MSIL has started the export of e-Vitara and also launched Victoris, a new model in the SUV segment. Taking these points into consideration, we revise our FY27/FY28 EPS estimates upwards by 5.5%/6.9% and arrive at our target price of INR 15,200. We value the company at 24x (previously 22x) on the average FY27/28E EPS and change our rating to REDUCE from ADD.

Financials:

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131