2025-09-16 10:26:04 am | Source: Choice Broking Ltd

Buy Mahindra & Mahindra Ltd for the Target Rs.4,450by Choice Broking Ltd

View and Valuation:

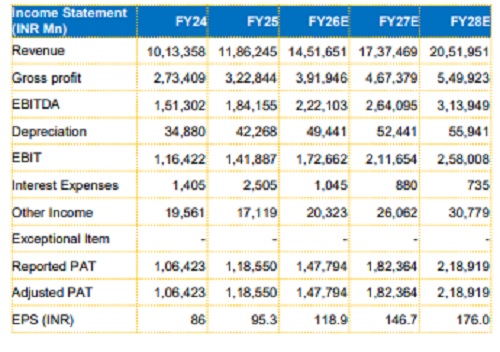

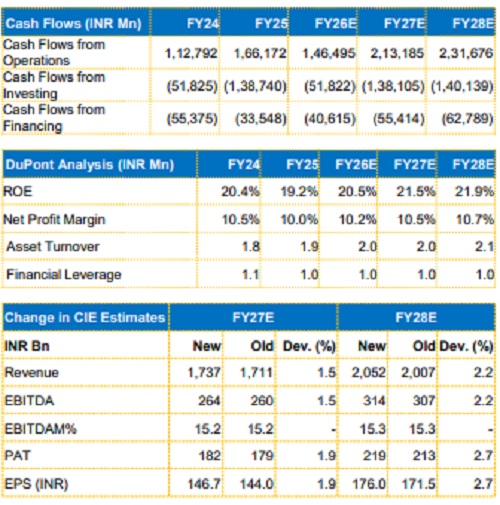

MM is a major beneficiary of the GST rate cuts, with these changes positively impacting all the segments of the company such as PV, CV and tractor. Around 95% of MM’s portfolio is set to benefit due to these rate cuts. On account of this, we revise our FY27/FY28 EPS estimates upwards by 1.9%/2.7% and arrive at our target price of INR 4,450. We value the company at 25x (maintained) on the average FY27/28E EPS, along with subsidiary valuation. We maintain our BUY rating on the stock.

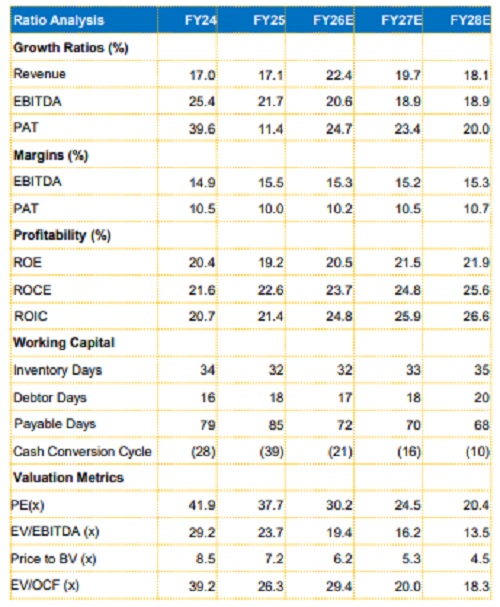

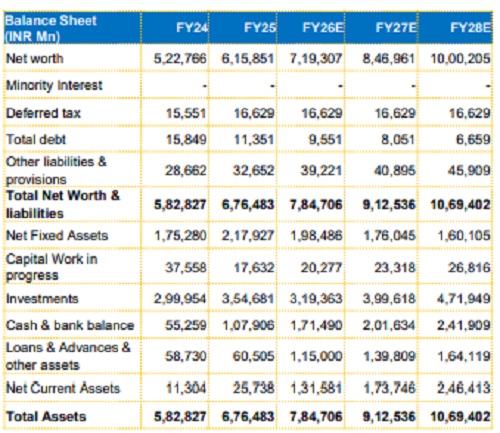

Financials:

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Ram Kapoor reveals his `real job` is `taking care` o...

Coimbatore Corporation to launch rooftop garden as p...

Quote on Market by by Mr. Vikram Kasat, Head - Advis...

Buy Gabriel India Ltd for the Target Rs. 1,125by Cho...

Technical Forecast : Nifty consolidates near 25100 z...

50,000 screenings of `Chalo Jeete Hain` on PM Narend...

Buy Fiem Industries Ltd for the Target Rs. 2,200 by ...

India`s merchandise exports rise 6.71% to $35.1 bill...

Kotak Mutual Fund`s Wake-Up Call on Quick Money Addi...

Buy Endurance Technologies Ltd for the Target Rs.640...