Buy Marico Ltd for the Target Rs.900 by Motilal Oswal Financial Services Ltd

Limited impact of geopolitical headwinds; low risk of an earnings cut

* The ongoing geopolitical challenges, if sustained, are expected to have huge bearings on cost inflation (more specifically on crude derivatives) across most of the FMCG companies. Besides raw material availability issues, a weak rupee is also expected to increase import costs for these companies. In this context, Marico appears relatively less affected by the overall RM volatility vs. its FMCG peers . Copra accounts for ~50% of Marico’s raw material basket, and it is currently witnessing a deflationary trend (with prices having corrected by 40% from their peak). Further, crude derivatives (including packaging) constitute 18-20% of total raw materials, resulting in a relatively lower impact than that faced by Marico’s peers. After registering 130% inflation over the past two years, copra prices are expected to continue their deflationary trend. Consequently, Marico is among the few companies where operating margins are projected to expand in FY27. Management has guided a base case EBITDA margin expansion of 150-200bp in FY27, and we believe this guidance remains achievable in the current environment.

* Moreover, Marico has been one of the few FMCG companies successfully expanding its non-core businesses. The company is steadily shifting its focus toward foods and premium personal care (targeting a 20–25% CAGR), with digital brands (e.g., Beardo and Plix) scaling well and improving profitability. Management aims to increase the contribution from foods and digital-first brands to ~33% of domestic revenue (up from ~25% currently). Such initiatives will help the company navigate macro calamities.

* Marico has been one of the best-performing stocks among FMCG peers during the last two years, delivering a 50% return. We reiterate our BUY rating on the stock with a TP of INR900 (premised on 50x P/E on FY28).

Resilient demand trends; minimal impact of geopolitical uncertainties

* Marico continues to witness resilient demand trends. The India business has delivered high single-digit volume growth and ~30% value growth in 9MFY26, outperforming most FMCG peers. The international business (~25% of revenue) grew ~18% in 9MFY26, driven by broad-based performance across geographies. The impact of ongoing geopolitical uncertainties remains limited, given low exposure to MENA (less than 5% of revenue).

* The demand trends are largely stable in 4Q, with no material disruption from gas supply issues due to the ongoing geopolitical uncertainties. The GST rate reduction has supported consumption, and this benefit is likely to continue into FY27, aiding demand recovery. Management remains confident in delivering 600 double-digit growth over the medium term.

India's core business essential with strong market leadership

* Parachute coconut oil: The Parachute franchise witnessed muted volume performance (-1% 3Q and -2% in 9M) due to a spike in copra prices. However, the segment delivered strong value growth (+50% in 3Q and 45% in 9M), driven by price hikes and selective grammage reduction. This led to a significant divergence between value and volume growth, which is expected to normalize as copra prices correct. With copra prices correcting meaningfully (~40% from peak), the company is likely to implement price reductions, which should support a gradual recovery in volumes and consumption trends.

* Saffola edible oil: The segment reported a relatively subdued performance, with flat value growth and a marginal dip in 3Q volumes, reflecting the impact of prior price rises and a softer consumption environment. The segment continues to face demand sensitivity due to pricing volatility; however, the company is focusing on premium offerings and health-oriented positioning, which are expected to support the gradual recovery. The performance is also hit by competitive intensity and consumer downtrading in certain segments.

* Value-added hair oil (VAHO): It has delivered the healthy revenue growth (29% YoY in 3Q) and gained ~170bp market share. Growth is led by premiumization, rural expansion under Project SETU, and improved distribution reach, with the segment likely to sustain double-digit growth over the medium term.

Evolving from a legacy FMCG to a digital and premium portfolio

* Marico is steadily transitioning from a traditional FMCG player toward a more digital-first and premium-focused consumer company. The portfolio is gradually shifting away from core categories such as coconut oil and edible oils toward higher-growth segments, including value-added foods, premium personal care, and digital-first brands. This transformation is aided by targeted acquisitions, strong operational discipline, synergy-led scale benefits, and prudent capital allocation within a scalable operating framework. Going forward, the company aims to deliver double-digit growth, driven by steady expansion in the core portfolio and faster, strong double-digit growth in its digital-first businesses.

* The company is steadily shifting its focus toward foods and premium personal care (targeting a 20–25% CAGR), with digital brands (e.g., Beardo and Plix) scaling well and improving profitability. Management aims to increase the contribution from foods and digital-first brands to ~33% of domestic revenue (up from ~25% currently).

* Marico is strengthening its portfolio through inorganic growth (refer to Exhibit 9). Recent acquisitions (4700BC, Cosmix, and Candid) are expected to contribute ~5% to FY30 revenues. Distribution expansion through Project SETU and rising traction in quick commerce are additional growth levers.

Food segment: Building a scalable high-growth engine

* Marico continues to build its food portfolio (refer to Exhibit 6) as a key longterm growth engine, with a focus on premium snacking, health & wellness, and modern breakfast categories. The segment reported moderate growth (5% in 3QFY26), impacted by ongoing portfolio rationalization and exit from lowmargin SKUs, aimed at improving the quality of growth.

* Despite near-term moderation, the company aspires to deliver a 20-25% CAGR in the foods segment. The segment has surpassed the revenue of INR9b in FY25 (5x that of FY20) and is expected to scale to ~9x FY20 levels by FY27 and ~15x by FY30 (refer to Exhibit 8). The growth is supported by strong traction in core brands such as True Elements, Saffola Oats, and Saffola Soya. In addition, recent acquisitions such as 4700BC (ARR of ~INR1.4b) and Cosmix (ARR of ~INR1b) are expected to scale 3.0–3.5x by FY30, further strengthening the portfolio.

* Operational improvements, including supply chain efficiencies and GTM refinements, have led to ~1,000bp gross margin expansion over the last two years, with further gradual improvement expected. While the company has a strong presence in modern trade and e-commerce, expanding general trade penetration remains a key growth lever.

Digital & D2C portfolio: Strong growth momentum

* Marico has built a strong portfolio of digital-first and D2C brands, including Beardo, Plix, Just Herbs, and True Elements . The company is focusing on high-growth categories such as male grooming, plant-based skincare, Ayurveda, and dermatology-led products. Growth is driven by strong consumer engagement, high repeat purchases, and increasing traction in ecommerce and quick commerce channels. In FY26, the premium personal care portfolio is expected to exit at an ARR of ~INR3.5b, while digital-first brands are likely to surpass an ARR of INR10b.

* Key brands have delivered robust growth over the last few years. Beardo has scaled ~5x over FY21-26 (~INR3.5b in FY26E). Plix has also witnessed strong momentum, with revenue scaling ~6x since FY24 (INR9b in FY26E). The recently acquired Candid brand (ARR of INR1b) is anticipated to scale ~3x over FY25-30. The digital-first personal care (PPC) segment is on track to deliver double-digit EBITDA margins by FY27, with a gradual improvement to mid-teen levels over the medium term.

International business driving growth; diversification reducing risk

* Marico’s international business reported strong growth of ~18% in INR terms during 9MFY26, driven by broad-based performance across key markets. The segment is expected to remain a key growth driver, supported by a gradual shift towards premium personal care and digital-first portfolios in core regions such as Vietnam, Bangladesh, and the Middle East.

* Marico is also focusing on reducing concentration risk through geographical and category diversification, while scaling up higher-margin segments within the portfolio. The increasing contribution from premium products and organized trade channels is likely to support margin improvement over the medium term. Despite ongoing geopolitical uncertainties, the overall impact on Marico remains limited, given its relatively low exposure to the MENA region.

EBITDA margin outlook improving

* Marico’s EBITDA margin dipped ~300bp YoY in 9MFY26 mainly due to a spike in copra prices, while the company did not fully pass on the cost increase through price hikes. Going forward, management expects margins to improve 150-200bp in FY27, supported by easing copra prices (which have declined ~40% from their peak), a higher share of premium and value-added products, and operating leverage from scaling newer businesses.

* However, while some pressure may persist due to inflation in select raw materials amid ongoing geopolitical uncertainties, Marico remains relatively less impacted by overall RM volatility compared to other FMCG peers.This is primarily because ~50% of its raw material basket is copra, which is currently witnessing a deflationary trend. We model an EBITDA margin of 18.8% in FY27 and 19.1% in FY28 (vs. 17.1% in FY26E).

Valuation and view

* The company is on track to deliver ~25% consolidated revenue growth in FY26, driven by pricing, expanded direct reach, and strong momentum across core categories as well as newer growth engines, such as foods and premium personal care.

* To improve its distribution reach, Marico has also started Project SETU, which helps drive growth in GT through a transformative expansion of its direct reach.

* This project is designed to drive growth by deepening market penetration and strengthening Marico’s presence across India. With these strategic initiatives in place, the company is focused on ensuring long-term profitability and further diversifying its business portfolio.

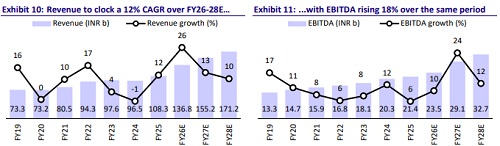

* We model a 12%/18%/16% revenue/EBITDA/APAT CAGR during FY26-28E. We reiterate our BUY rating with a TP of INR900 (based on 50x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041