Buy Marico Ltd For Target Rs. 850 by Motilal Oswal Financial Services Ltd

* Domestic business saw steady momentum in Jul-Aug; saw transitory impact of disruption in trade channels and CSD ahead of the implementation of new GST rates in Sep.

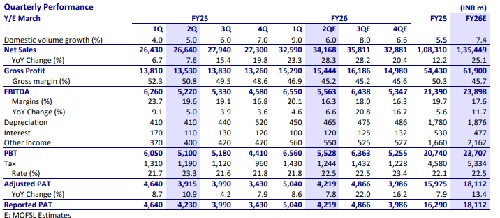

* We expect 28% consol. revenue growth and ~6% domestic volume growth. The high pricing contribution is driven largely by price hikes in Parachute.

* Gross margins expected to contract 560bp YoY to 45.2% given high base and rise in RM prices. Operating margins are expected to contract 330bp YoY to 16.3%.

* Parachute should see low-single-digit decline in volumes amid unprecedented hyperinflation in input costs and pricing conditions. After normalizing for ml reductions in lieu of price increases, volume is expected to be flat in 2Q.

* Saffola Oils expected to deliver flat volumes on a high base, and revenue growth in the high teens. VAHO should deliver high-teen growth.

* The International business is expected to deliver ~20% revenue CC growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...