2026-01-10 04:24:41 pm | Source: Motilal Oswal Financial Services Ltd

Buy LT Foods Ltd for the Target Rs. 550 by Motilal Oswal Financial Services Ltd

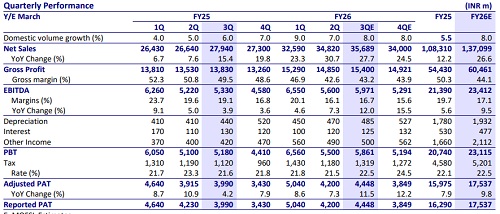

* We expect consolidated sales to grow ~21% YoY, primarily driven by volume growth

* EBITDA margin expected to remain constant YoY at 11% in 3QFY26.

* We expect the International operations of Specialty Rice to grow ~29% YoY due to the change in base resulting from the acquisition of Golden Star.

* Organic segment’s gross margins are expected to decline 960bps YoY in 3QFY26, impacted by outsourcing operations due to new plant commissioning in Europe.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Perspective on Markets by Karthick Jonagadla, invest...

Buy Gold Above 148100 SL BELOW 147000 TGT 149700/150...

Big Breaking! MeitY pulls two E-Rickshaw prank apps ...

Odisha Governor Hari Babu Kambhampati offers prayers...

India-Japan strengthen ties with 129 new MoUs during...

Haryana CM Nayab Saini honours Super-100 students cl...

`Aim To Increase Japanese Investment In India Beyond...

Hindustan Zinc jumps as its mined metal production r...

Zydus Lifesciences soars on inking pact with Apollo ...

Shivalik Bimetal Controls climbs as its arm gets con...