Buy L&T Technology Services Ltd for Target Rs. 4,350 by Choice Institutional Equities

Reset Behind, Strong Recovery Outlook; Maintain BUY LTTS is well-positioned for FY27E recovery, supported by sustained large-deal momentum, improving traction across core segments and early stabilisation in Mobility and Tech. Ongoing portfolio recalibration (exit from low-margin and nonstrategic businesses) is driving improved revenue quality and margin expansion, with further upside from AI-led delivery and scaling of high-value engagements. While near-term growth remains modest amid portfolio pruning, strong deal wins and ramp-ups and improving execution underpins recovery visibility. We see a credible path to mid-16% EBITM by Q4FY27E. We roll forward to FY28E EPS, maintain a 25x PE multiple and derive a TP of INR 4,350; retain BUY rating, supported by industry-leading growth and margin recovery.

Revenue Miss due to SWC Disinvestment; EBITM Beats; PAT in Line

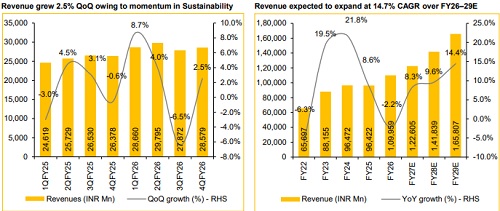

* Revenue for Q4FY26 was USD 305.9 Mn, down 1.7% QoQ while it was up 0.3% YoY (vs CIE est. at USD 323.6 Mn). In INR terms, revenues came in at INR 28.5 Bn, up 2.5% QoQ and up 8.3% YoY (vs CIE est. at INR 29.1 Bn)

* EBIT for Q4FY26 came in at INR 4.3 Bn, up 5.5% QoQ and 23.6% YoY (vs CIE est. at INR 4.1 Bn). EBITM was up 42 bps QoQ and 188 bps YoY to 15.2% (vs CIE est. at 14.2%)

* PAT for Q4FY26 stood at INR 3.3 Bn, up 9.7% QoQ and 6.8% YoY (vs CIE est. at INR 3.2 Bn)

Portfolio Rationalisation Weighs on Revenue; Segment Traction Improves Visibility: Q4FY26 revenue stood at USD 306 Mn, down 1.7% QoQ, reflecting continued impact of purposeful portfolio rationalisation (SWC disinvestment and exit of a couple of clients) aimed at improving revenue quality. Segmentally, Sustainability remained the key growth driver with double-digit momentum and strong deal execution, while Mobility stabilised sequentially with early recovery signs led by North America Auto and SDV traction, supported by improving deal pipeline. Tech saw near-term softness owing to exit from non-strategic businesses, though underlying traction across Semicon, Medtech and Platformled offering remains intact with ramp-ups expected ahead. Strong deal wins and a robust pipeline provide improving revenue visibility as portfolio rationalisation largely concludes and deal ramp-ups accelerate. We expect near-term revenue softness as transitory, with the portfolio reset laying the foundation for stronger, quality-led growth ahead

Margin Expands; Path to Mid-16% EBITM by Q4FY27E Intact: EBITM improved 40 bps QoQ to 15.2% in Q4, marking the second consecutive quarter of expansion driven by portfolio pruning, favourable mix and cost discipline. Margin trajectory remains supported by AI-led delivery, SG&A rationalisation and increasing share of high-margin engineering intelligence (EI) work. Large deal win remains strong at USD 855 Mn in FY26 (+40% YoY) with Q4 Large deal TCV at USD 182 Mn, providing healthy revenue visibility. Hiring momentum and continued investments in AI capabilities (~65% workforce AI trained) indicate readiness for deal ramp-ups. As a part of ‘Lakshya FY31,’ the management now targets delivery of 13% to 15% CAGR in the next 5 years, with mid-16% EBITM by Q4FY27E. We see margin expansion as structurally intact, with improving mix and disciplined execution supporting a credible path to midteen profitability

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131