Buy Krishna Institute of Medical Sciences Ltd For the Target Rs. 710 By the Axis securites

Recommendation Rationale

Operational Performance: Consolidated occupancy declined by 1,091 bps YoY and 610 bps QoQ, settling at 50.7%. However, ARPOB saw a 25.1% YoY increase and grew 0.5% sequentially to Rs 38,472 in Q3FY25. This growth was supported by new beds, an improved case mix, and revised pricing through TPA negotiations.

Margins and Profitability: EBITDA margins remained constant at 24.2% YoY but declined 38 bps QoQ due to higher OPEX. Reported PAT rose 20.8% YoY to Rs 92 Cr, benefiting from increased operating profitability.

Regional Performance: While the Telangana and Andhra clusters experienced a decline in occupancy, ARPOB growth remained strong, rising ~15% and ~24%, respectively. These clusters remain the largest revenue contributors, with matured assets in Telangana and Andhra Pradesh recording ARPOB of Rs 63,363 and Rs 21,175, respectively. This growth was driven by a favourable case mix and reduced ALOs.

Sector Outlook: Positive

Company Outlook & Guidance: KIMS is poised for continued growth, driven by its strategic expansions, improving case mix, and increasing ARPOB. While occupancy levels have temporarily dropped, the company’s focus on high-value specialties, operational efficiencies, and geographical expansion should support long-term profitability. In the near term, the company expects Nashik Hospital to break even by Q2–Q3 FY26, while Thane and Bangalore hospitals are set to commence operations by FY25-end. The recently opened Guntur and Kollam hospitals will contribute to revenue growth, though initial ramp-up costs may weigh on margins. Looking ahead, KIMS is making a significant push into Kerala, aiming to add 2,000 beds over the next 6–8 years, capitalising on the state’s high hospitalisation rate and strong demand for premium healthcare services. Additionally, management remains cautious about sustaining its current EBITDA margins (~25%), as industry-level normalisation is expected.

Current Valuation: EV/EBITDA 23x for FY27E EBITDA

Current TP: Rs 710/share (Earlier TP: Rs 615/share)

Recommendation: BUY

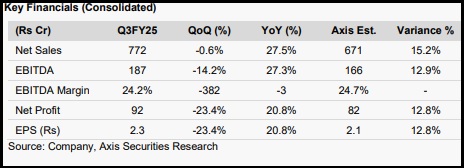

Financial Performance KIMS delivered a strong performance in Q3FY25, driven primarily by higher ARPOB growth despite a decline in occupancy. Consolidated occupancy declined by 1,091 bps YoY and 610 bps QoQ, settling at 50.7%. However, ARPOB saw a 25.1% YoY increase and 0.5% sequentially to Rs 38,472 in Q3FY25. This growth was supported by new beds, an improved case mix, and revised pricing through TPA negotiations.

Financial Performance (Cont’d) KIMS delivered a strong performance in Q3FY25, driven primarily by higher ARPOB growth despite a decline in occupancy. Consolidated occupancy declined by 1,091 bps YoY and 610 bps QoQ, settling at 50.7%. However, ARPOB saw a 25.1% YoY increase and 0.5% sequentially to Rs 38,472 in Q3FY25. This growth was supported by new beds, an improved case mix, and revised pricing through TPA negotiations. The company’s revenue grew 27.5% YoY, while realisations increased 25.1% YoY. The drop in occupancy was primarily due to the inclusion of Vizag’s Queen Hospital (300 beds). Further, occupancies declined in the Telangana and Andhra clusters. Additionally, the Maharashtra cluster, particularly Nagpur, experienced a seasonal impact, leading to a revenue decline, which may have also contributed to the lower occupancy rate. On a like-for-like basis, occupancy levels stand at approximately 53%. EBITDA margins remained constant at 24.2% YoY but declined 38 bps QoQ, impacted by higher opex. Reported PAT rose 20.8% YoY to Rs 92 Cr, benefiting from increased operating profitability. While the Telangana and Andhra clusters experienced a decline in occupancy, ARPOB growth remained strong, rising ~15% and ~24%, respectively. These two clusters remain the largest revenue contributors, with matured assets in Telangana and Andhra Pradesh recording ARPOB of Rs 63,363 and Rs 21,175, respectively. This growth was driven by a favourable case mix and reduced ALOs. Furthermore, the Maharashtra cluster showed a decline in occupancy along with degrowth in ARPOB on a YoY basis. KIMS has expanded its hospital network, with several new facilities commencing operations. Nashik Hospital began operations in Q2FY25, with management expecting it to break even by Q2–Q3FY26. Additionally, the KIMS SIKHARA hospital in Guntur (200 beds) is set to be inaugurated on February 12, 2025, marking a significant expansion in Andhra Pradesh. The company has also entered Kerala with the VIMS Valiyath Institute of Medical Sciences (300 beds) in Kollam, making it the second KIMS hospital in the state. Further expansions include upcoming hospitals in Thane and Bangalore, both expected to commence operations by the end of FY25. The management remains committed to scaling up its presence in Kerala, targeting 2,000 beds over the next 6–8 years, leveraging the state’s high demand for quality healthcare. Notably, revenue in significant therapeutic areas such as cardiac, ortho, and gastric surged by 20%, 27%, and 43% YoY, respectively, while Onco registered a 53% YoY growth. However, a key concern for KIMS is its higher-than-industry operating margins of approximately 25%, which may be difficult to sustain as its ARPOB remains lower than the industry average of Rs 54,000.

Outlook KIMS is positioned for sustained growth, driven by strategic expansions, an improving case mix, and rising ARPOB. While occupancy levels have seen a temporary dip, the company’s focus on high-value specialties, operational efficiencies, and geographical expansion should support long-term profitability. In the near term, Nashik Hospital is expected to break even by Q2–Q3FY26, while Thane and Bangalore hospitals are set to commence operations by FY25-end. The recently opened Guntur and Kollam hospitals will contribute to revenue growth, though initial ramp-up costs may impact margins. Looking ahead, KIMS is making a significant push into Kerala, aiming to add 2,000 beds over the next 6–8 years, leveraging the state’s high hospitalisation rate and strong demand for premium healthcare services. Additionally, management remains cautious about sustaining its current EBITDA margins (~25%) as industry-level normalisation is anticipated.

Valuation & Recommendation: In light of increasing ARPOB and the incremental supply of beds, which is expected to lead to more substantial cash flow, we maintain our BUY rating on the stock with a target price of Rs 710/share with a valuation of 23x EV/EBITDA for FY27E. The TP implies an upside potential of 10% from the CMP.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633