2025-10-16 11:54:39 am | Source: Motilal Oswal Financial Services Ltd

Buy Kalpataru Projects International Ltd for the Target Rs. 1,450 by Motilal Oswal Financial Services Ltd

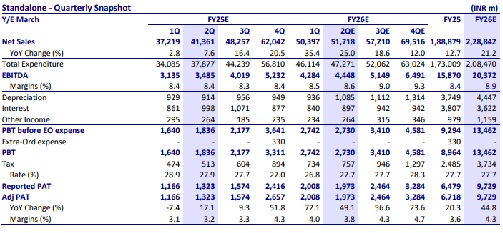

* We expect revenue growth of 25% YoY on strong execution across segments such as T&D, B&F, and O&G, barring the water and railway segment, which is still slow.

* We expect EBITDA margin of 8.6% (+20bp YoY/+10bp QoQ) and gradual improvement through the remainder of FY26.

* We will monitor the working capital cycle closely. The payment status of water projects will also remain a focus area.

* Key monitorables include execution ramp-up, margin trajectory, customer collections, and outlook on the urban infra and railways division.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

`Aim To Increase Japanese Investment In India Beyond...

Hindustan Zinc jumps as its mined metal production r...

Zydus Lifesciences soars on inking pact with Apollo ...

Shivalik Bimetal Controls climbs as its arm gets con...

Central Bank of India rises on posting 29% growth in...

Advisor to PM, Tarun Kapoor, highlights importance o...

State reforms to triple India`s commercial and indus...

MoS External Affairs Pabitra Margherita leaves resid...

Over 2.5 lakh Aadhaar email updates recorded in 1st ...

Reliance Industries Executive Director, Anant Ambani...